- 20 Feb, 2024

Chances Of Mortgage Approval With A 665 Credit Score

Can you buy a house with a 665 credit score: Should you improve it?

As a 665 credit scorer, you can certainly get into the process of borrowing money. But, you should know that a credit score that falls anywhere between the 580-669 range is considered a FAIR credit.

In today's blog, we will help you understand the details of a 665 credit score and share practical tips for improvement.

Also, if you're on the hunt for a new place and worried about your credit, we've got your back with expert suggestions on finding houses for rent no credit check required.

What does a 665 credit score mean?

A credit score 665 falls under the category of a “fair” range and it is not considered a good credit score by FICO.

Now, if you’re in this category, you might be referred to as a “subprime” borrower.

What that means is that lenders could see you as a bit more of a risk.

But hey, as an individual with a 665 credit score, you’re just 5 points away from achieving a good credit score and qualifying as a low-risk borrower. With some smart financial moves, you can still work your way up to better scores!

👇 Scroll to see how.

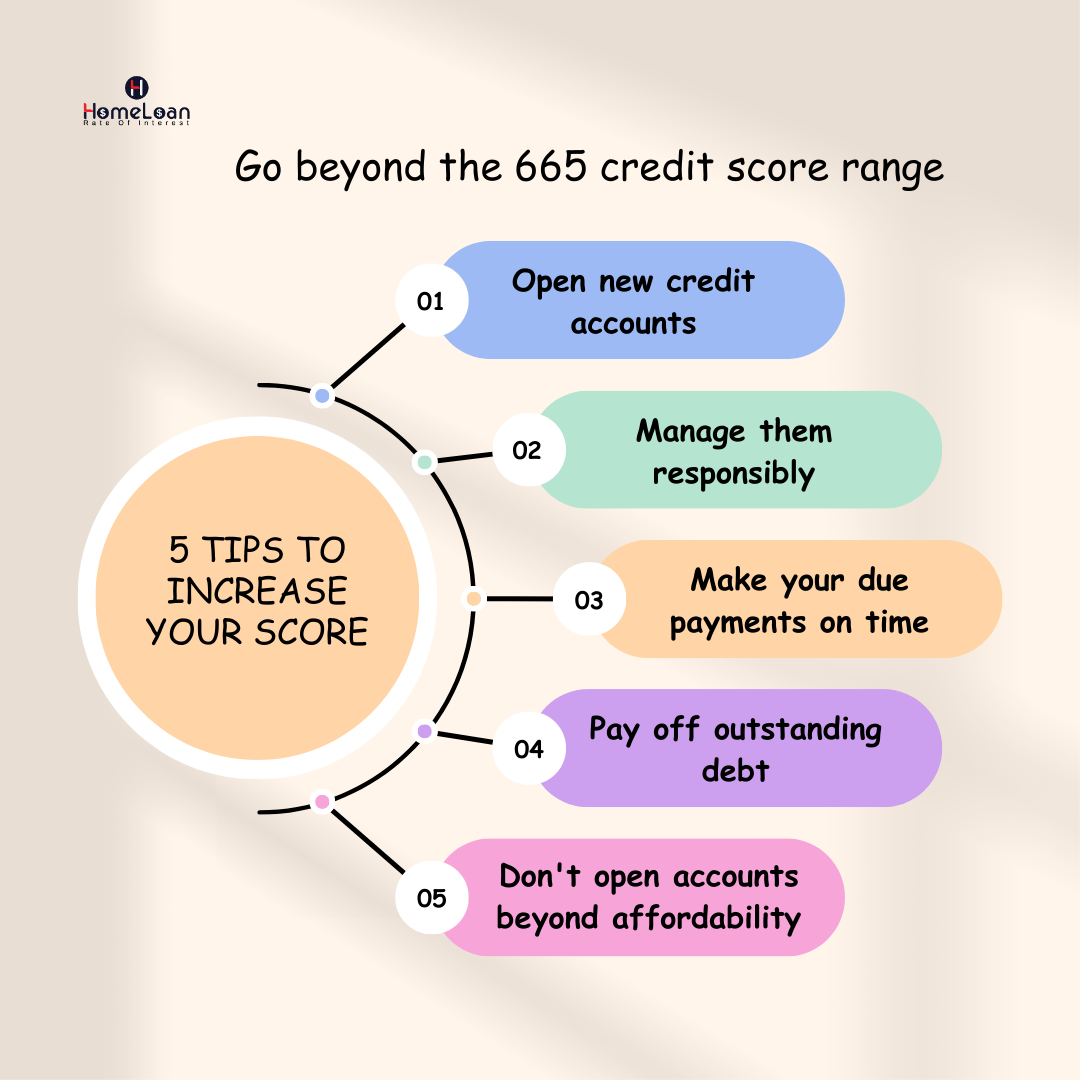

5 ways to improve your 665 credit score

When it comes to applying for a new credit card or loan, having a 665 credit score may pose a few challenges. It's not as smooth sailing as it is for borrowers with credit scores of 670 and above.

So, what does it take to go up the ladder and get those 5 extra credit points? How can you be among the 70% of consumers, whose FICO scores are higher than the 665 range?

↓ Follow these steps to upgrade your credit report ↓

-

Have a credit portfolio

If you have a low credit score, or you’re just starting out, try to get a rewards credit card that has no annual fee. But as a 665 credit scorer, we are sure you might have a credit history.

Try to get a few other accounts in your name, and manage them responsibly to raise your credit points.

Also, becoming an authorized user on someone else's credit card can get you a score upgrade.

-

Never miss a payment

Making payments on time is one of the most important things you can do to improve your credit scores. If you continue to miss the due date by more than 29 days, there are chances your credit score can hit rock bottom!

Set up automatic payments for at least the minimum amount to be paid to avoid this. If you're struggling to pay a bill, talk to your credit card issuer to explore options that fit your payment schedule.

Also, if you have multiple accounts, manage them responsibly. Track the due dates properly, plan your payments, and repay the borrowed amount.

-

Settle outstanding payments

In case you’re unable to pay the bills on time due to various financial obligations, it's time to play catch-up.

Beware of additional late fees if you continue to delay your payments. Not just that, a late payment can be reflected on your credit report for up to 7 years. It’s not good for someone who wants to see those good credit score numbers.

So, it’s best to avoid late payments as much as possible. Even if you happen to have some dues, settle them all before you make your next credit purchase.

-

Reduce revolving account balances

Have you heard about the credit utilization ratio? Lenders look at this ratio to see if you're handling your debts responsibly. The lower the percentage, the better it generally looks to them.

Here’s an expert tip by Beverly Harzog (Credit Card Expert & Personal Finance Author) –

She says, “If you really want to boost your score a lot, keep your credit utilization ratio under 10%.”

It means that you’re using lower credit than the total credit available to you. So, keeping this number low can be a smart move for your financial health!

Now, let's talk about credit cards and lines of credit. Having a high balance on these accounts hurts your credit scores. Try to keep the balance low compared to your credit limit.

-

Limit opening new accounts

Opening new accounts can build a great credit profile, but don't overdo it. Each time you apply for credit, a hard inquiry is raised on your profile. This can lower your credit scores. So don’t open too many accounts that you can’t handle or manage.

Try to keep new applications to a minimum, unless you're shopping for specific loans like a car loan or mortgage. In those cases, multiple applications close together might be overlooked by the credit-scoring models.

Make tiny little changes to your spending habits, monitor your credit dues, and repay your borrowed money on time, so that you can get those extra 5 points and go from fair to good.

Would you like to know how your credit scores are calculated? Stick around to check it out!

How’s your credit score calculated?

You might know by now that a credit score is used to measure your risk as a borrower.

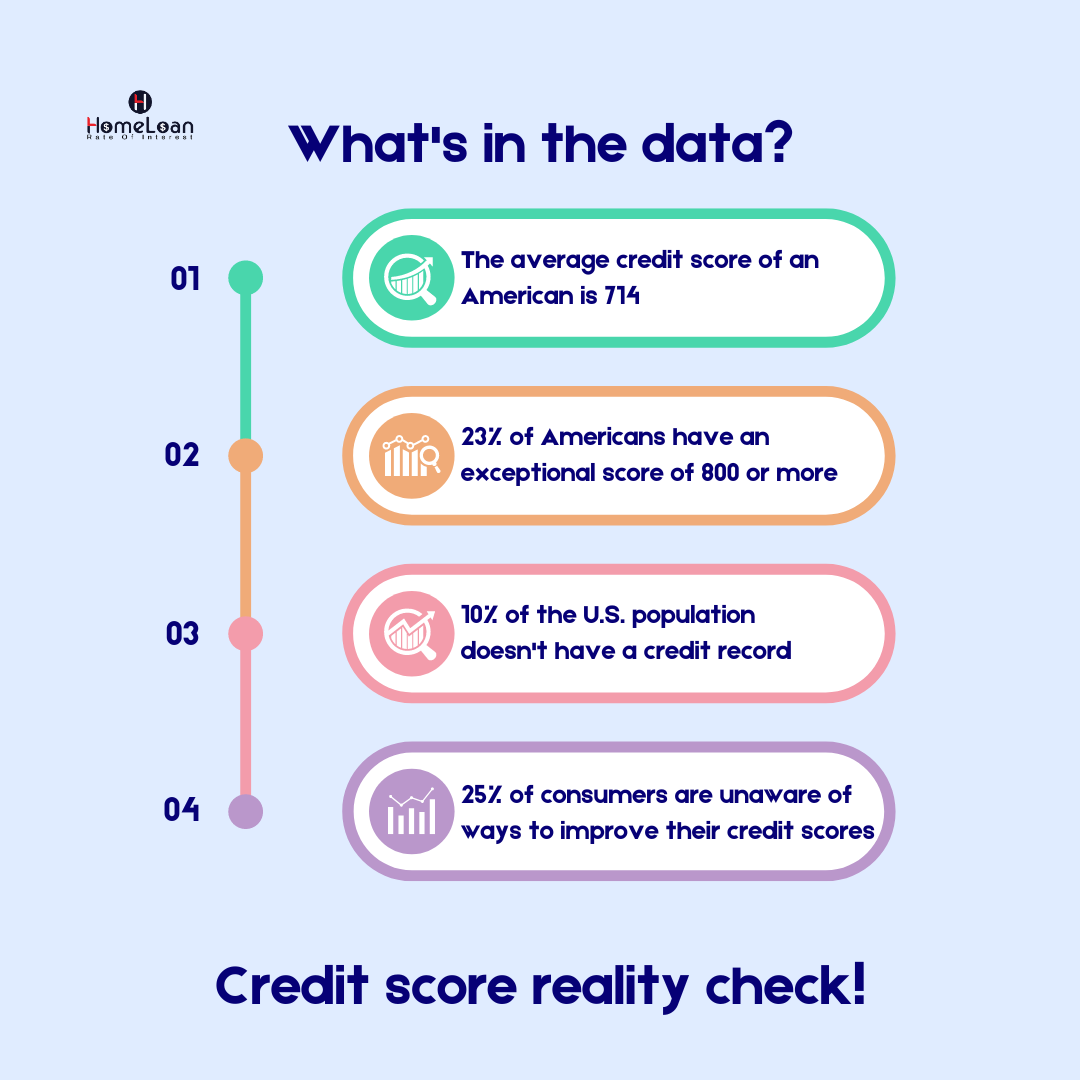

Did you know that 90% of U.S. lenders use FICO scores as a base to evaluate the borrower’s potential to repay the loans?

If you’re a first time homebuyer and you have a credit score of 665 who’s looking to boost your chances of getting a mortgage or an auto loan, understanding how credit scoring works is key.

It helps you handle your credit profile in a way that makes lenders more likely to say "yes" to you.

Here are the 5 aspects of your credit score, ranked based on the weightage (out of 100%)

-

Payment history (35%)

This category checks if you’ve completed your due payments on time or if it’s still pending. They check your consistency in paying the bills on time.

But, if you've had moments where you were a bit late, or if you've faced more serious things like bankruptcy, collections, or delinquencies, the scoring might go down.

It’s simple –

Good payment history = Good credit score

Late payments or over-utilization of credit = Lower credit score

-

Amount owed (30%)

The total amount you owe on your loans and credit cards is a key factor. If you're someone who likes to stay within your credit limits and only use credit when absolutely necessary, this approach can be beneficial for your credit score.

However, if you're used to the habit of using your credit for various expenses and run the risk of exceeding your credit limit, it could label you as a higher-risk borrower. This may not work in your favor.

Moreover, if this pattern repeats across multiple accounts, it can have a negative impact on your credit scores. So you need to manage your credit responsibly to maintain a positive credit profile.

-

Length of credit history (15%)

How long you've had your credit accounts matters. If you've had them for a long time and always paid on time, that's a good thing.

Let’s say a borrower has been paying his bills on time for 20 years – that looks impressive to lenders, right?

They prefer someone with a long, reliable credit history over someone who's only been on time for a couple of years with a not-so-good credit history.

-

A mix of different credit accounts (10%)

10% of your score consists of different types of credit accounts you have. A mix of home loans, auto loans, retail & travel credit cards, will have a positive impact on your credit score 665.

-

New credit (10%)

A few individuals tend to go the extra mile and open a lot of new credit accounts thinking it will boost their credit scores. But, no!

It works the other way around. It doesn't directly harm your score, but here's the catch – if you've been a bit all over the place with your existing credit accounts and then decide to open new ones, things can get a bit tricky.

It's like trying to juggle too many things at once – things might not go as smoothly as you hoped!

Now you know how those three-digit numbers are calculated and given to you!

So, the only way to get your scores to the level of “good” is by showing your lenders that they can trust you and that can be shown through your responsible credit behavior .

Stop focusing only on your credit scores. Use your time efficiently to research different loan options while working on your credit!

Click here to get home loan quotes from top lenders in your county.

Next up, switching gears a bit we will be discussing a related topic – Houses for rent no credit check.

Let’s say you’re in dire need of a house to move into and you start looking for rental properties or you simply don’t want to put so much effort into getting your scores on top of the table. Do you still need to go through credit checks?

Unfortunately, yes. Many landlords ask for your credit report to check if you will be paying your rent and utility bills on time.

But, there is a way to find houses for rent without a credit check.

How to get houses for rent with no credit check?

Don’t have a credit history? Does your credit fall under the “fair” range on the FICO scale? No worries. There are ways to get out of this and get your rental agreement approved.

-

Rent from an Individual Owner

Some private landlords may allow you to rent without a credit history. Be cautious of scams, and avoid upfront payments or wire transfers. However, before moving ahead you need to prove your income stability.

-

Move in immediately

Landlords may approve if you are ready to move in immediately. Empty apartments cost landlords money, so it's an incentive for them.

-

Prove your income

One thing landlords assess apart from your credit score is your income stability. This is because you need a certain level of stability to cover your rental expenses.

💡PRO TIP – Keep your rent below one-third of your take-home pay.

-

Get a supporting co-signer

If nothing of the above works for you, consider approaching a co-signer with good credit or if you’re planning to bring in a roommate with you, they can be your cosigner as well.

Also, you can save on huge rental and living expenses, as you can share it with the person who has agreed to move in with you.

These are some of the ways you can get houses for rent no credit check required. You can choose to skip your credit only if you’re in urgent need of getting a rental house.

If you want to get better deals, and the power to negotiate, try to improve your 665 credit score using the tips listed above.

The bottom line

There's always room for improvement, and with the right strategies, individuals can enhance their creditworthiness and move towards enhancing the success rate of their credit and mortgage approvals.

Improving your credit scores can only get you closer to mortgage approvals, better interest rates and terms. So, go ahead and implement the tips given in this blog to get those 5 extra credit points.