- 05 Jan, 2024

VA Loan Vs. Conventional Loan - What Homebuyers Need to Know

Conventional Loan vs VA Loan: Detailed Comparison & What to Choose

Whether you’re an existing homeowner or moving into a new home for the first time, you might be on the lookout for a home loan to finance your home purchase.

In this blog, we will help you with just that. You will discover the main difference between conventional loan vs VA loan and also learn useful tips on how you can get a VA loan with bad credit.

VA loan uses & types

These loans are designed to benefit all veterans, service members, and their families. VA loans are backed by the U.S. Department of Veterans Affairs and help veterans purchase a home with little to zero down payment at competitive interest rates.

VA loans provide up to 100% financial assistance on the total value of a home. If you’re eligible, you have multiple options – the loan can be used to purchase/build a home, improve/repair your home, or you can refinance a mortgage.

If you’re planning on taking a VA loan, make sure you provide your lender with a COE, and a certificate of eligibility to prove your servicing time as a veteran.

Alright, we will explore the types of a VA loan next!

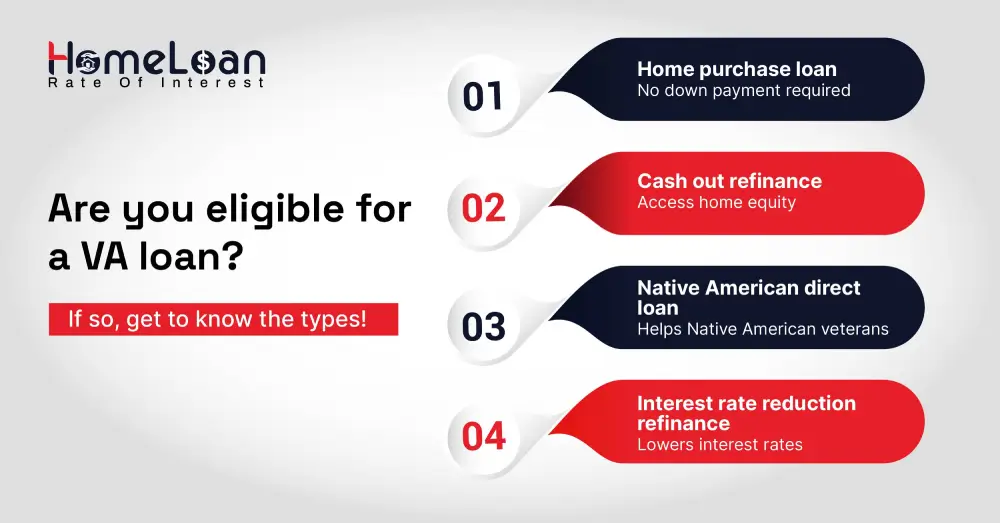

Types of VA loans

Just like every other mortgage out there, VA loans also offer a variety of choices for you to consider, tailored to your specific requirements. Here is a quick breakdown of the types:

-

Home purchase loan

These loans are designed to assist veterans in purchasing a home at competitive interest rates.

They do not require a down payment, making homeownership more accessible.

Unlike many conventional loans, VA home purchase loans typically do not require the borrowers to pay private mortgage insurance.

-

Cash-out refinance loans

This type of loan allows homeowners to borrow against the equity in their homes for various purposes such as debt consolidation, home improvements or to fund their kid’s schooling.

The new mortgage obtained through a cash-out refinance is for a larger amount than the previous mortgage.

-

Native American direct loan

This program is specifically designed to assist eligible Native American veterans in financing the purchase, construction, or improvement of homes on federal trust land.

These loans often come with reduced interest rates, providing additional financial benefits.

-

Interest rate reduction refinance loan

This is a VA loan to VA loan process allowing existing veteran homeowners to refinance their fixed rate mortgage at a lower rate of interest or convert their adjustable rate mortgage into a fixed rate mortgage.

Interest rate reduction refinance loan is aimed at helping borrowers obtain a lower interest rate.

Each type of VA loan serves a specific purpose. You have a variety of options now! Be it a home purchase, a home improvement, or a reduction in your interest rates, you are open to choosing any of the following.

But, hold on! Why don’t we also look into the conventional loan options and then decide what’s best for you? Sounds good! Well, scroll down then.

Conventional loan: Everything you need to know

Unlike VA, FHA, and USDA loans, conventional loans are not backed or insured by the U.S. government. They are offered by private lenders and require borrowers to pay an upfront down payment of a minimum of 3% to a maximum of 20% of a home’s purchase price.

The total down payment that you need to pay will be determined based on your financial history, credit score, and other factors that we will be discussing in the coming sections.

Although conventional loans are not backed directly by the U.S. government, two government-sponsored enterprises (Fannie Mae and Freddie Mac) set the guidelines and requirements for conventional loans.

If you want to get approval on a conventional loan, you’re required to maintain a strong credit history and income level. You get to lock in competitive rates and mortgage terms.

In addition to that, borrowers also have a level of flexibility when it comes to maximum loan amounts compared to government-backed loans.

Now, let's familiarize you with the different conventional loan options available before jumping to the comparison between VA loans vs conventional loans.

Types of conventional loans

Each type of conventional loan comes with its own requirements and offerings. Here’s a short explanation for you:

Conforming loans

To start with conforming home loans, they adhere to specific lending criteria established by government-sponsored entities (GSEs) like Fannie Mae and Freddie Mac.

The criteria include factors such as credit and income requirements, minimum down payments, debt-to-income ratios, and more.

They typically come with lower interest rates because lenders view them as lower risk due to their adherence to standard lending criteria.

There is a maximum limit set by Government-sponsored enterprises (GSEs) on conforming loans, and this limit can vary based on the location.

Non-conforming loans

Non-conforming loans on the other hand do not go by the guidelines or criteria set by Fannie Mae and Freddie Mac.

Interest rates for non-conforming loans are generally higher because they are considered riskier for lenders. Lenders might also require a larger down payment compared to conforming loans.

Eligibility for non-conforming loans can be more flexible as they’re underwritten manually, where an underwriter evaluates your documents to determine whether you qualify to borrow.

Fixed-rate and adjustable-rate mortgage

A fixed-rate mortgage maintains a constant interest rate throughout the entire loan term whereas adjustable-rate mortgages can change as per designated points once the initial fixed-rate period is done.

The fixed-rate option provides borrowers with predictability in monthly payments, making it easier to plan and budget over the long term.

With the adjustable-rate option, the monthly mortgage payments will be lower during the initial fixed-rate period but might fluctuate once the payments rise. This might increase the housing costs over time.

The most awaited part of the blog is right below! Let’s pick out the main differences between VA vs conventional loans.

Key differences between conventional loan vs VA loan

If you aim to secure the right mortgage, you need to examine the key factors to understand the differences. So, let’s get to the main highlight of today’s blog - VA vs conventional loan.

| Conventional loan | VA loan |

|---|---|

| 1. They can not just be used to purchase a primary residence, but also second homes, vacation homes, rentals, and investment properties. | 1. They can’t be used on any other property other than the primary home. |

| 2. The minimum credit score requirements vary from lender to lender. But, most lenders require a credit score of 620. | 2. As they are offered by the government, credit score requirements are not as strict as conventional loans. Even a score of 580 can qualify you for a VA loan. |

| 3. Lenders require borrowers to put down a minimum payment of 3% of the home’s purchase price for a successful approval. | 3. VA loans, on the contrary, don’t have any down payment requirements. But, if your credit score is low, lenders will require you to pay a minimum down payment. |

| 4. The main difference between conventional loan vs VA loan is the private mortgage insurance. The usual PMI for conventional is around 0.1% to 2% of the loan amount per year. | 4. VA loans don’t have a PMI requirement. But there’s something called a VA funding fee. They are similar to PMI and some veterans can be exempted from this fee. |

| 5. Your debt-to-income ratio should not be more than 45%. However, certain lenders allow a DTI of up to 50% as well. | 5. There are no specific DTI requirements and most of the lenders set their own requirements. Instead of a DTI, VA loan lenders look at other factors such as military benefits and credit scores. |

Before finalizing your choices, you need to weigh the differences between VA loans vs conventional loans.

Take time to understand what your financial goals are, and consult with mortgage professionals if you have questions so that they can give you the clarity you need.

Do you have your pick already? What are you waiting for? Get a quick quote and start your application with the Home Loan Rate of Interest.

But hey, what if your credit scores don’t meet lender requirements? Don’t worry even if you have a poor credit score. You can still get a VA loan with bad credit. Stay tuned as we share with you solutions below.

VA loan with bad credit?

Can you get a VA loan with bad credit? Yes, it is possible to secure a VA-backed home loan even if your credit score is not as shiny and attractive as 620.

Unlike some conventional loans, the Veterans Affairs (VA) itself does not establish a minimum credit score requirement for applicants. Instead, they ask their lenders to check the last 12 months' financial statements to assess your payment history.

If you’re still wondering whether a VA loan with bad credit is possible, you need to know that credit scores are not the only factors lenders assess your creditworthiness.

There are other compensating factors as well like – income requirements, ability to manage debts, military benefits, and more. But, it is wise to check with your lender if you qualify or not. If you still face any challenges, no worries. You can improve your scores! We’ll see how.

How to improve a bad credit score?

Improving a bad credit score is a confident decision but it requires dedication and strategic financial management. Here’s a quick sneak peek into ways you can improve your credit score.

-

Obtain free annual credit reports from major credit bureaus like – Equifax, Experian, and TransUnion.

-

Check if there are any reports for errors, inaccuracies, or fraudulent activity.

-

Prioritize making timely payments on all current debts you have.

-

Aim to lower credit card balances, this will lower your credit utilization ratio.

-

Finally, have patience, stay committed to maintaining healthy financial habits, and monitor your progress regularly.

If you’re on a mission to get the best rates and mortgage terms, improve your credit scores, and walk into the home of your dreams!

Next steps: What should you do?

The ball is in your court! Assess your needs, and know what kind of mortgage terms work well for you.

If you’re still in doubt, consult with a mortgage professional. They can provide personalized advice based on your specific situation, ensuring you make the best choice for your future home.

As a next step, once you have decided, you can go ahead and approach your lenders with all necessary documentation, follow their instructions, apply, wait for approval, review all the paperwork, and get the keys to your new home.