- 12 Oct, 2023

Is Now a Good Time to Secure a 30-Year FHA Mortgage? Analyzing Current Rates and Trends

Is FHA 30 year fixed rate mortgage the right option for you?

It is time to accept that the mortgage industry is competitive! If you’re a homeowner looking to invest in a real estate property or manifest your home ownership dreams, a 30 year FHA loan is a must-explore option. Watching out for future rates and assessing the current market trends will help you choose an appropriate 30 year mortgage.

In this blog, we will help you understand more about the FHA 30 year fixed rate options, along with factors influencing mortgage rates, and mortgage rate predictions for 2024. Let’s also discover more about your credit score factors, down payment options, and competitive interest rates.

In addition to this, we will learn more about mortgage insurance premiums to figure out why many first time homebuyers prefer a 30 year FHA mortgage. Hang in there to make the smart decision before getting hold of your keys. Let’s start now!

Fundamentals of FHA mortgages

FHA [Federal Housing Administration] is the most viable option for first time home buyers. An FHA loan is backed by the government. What makes an FHA loan an attractive option for home buyers is their credit score requirements. Not only that, the downpayment required is comparatively lower than a conventional loan.

If you are looking to get an FHA mortgage, you are required to pay mortgage insurance to ensure that the lenders are protected during times of uncertainty. We will find out how the mortgage insurance system works under the FHA 30 year fixed rate category in the coming sections.

All about FHA 30 year fixed rate mortgage

Taking out a mortgage involves being responsible for three decades to pay off and close the mortgage. As the name speaks for itself, the loan term is spread over 30 years and this extended period allows first time homeowners several advantages such as lower monthly payments, and options to qualify with lower credit scores.

Here are some key points to remember when it comes to FHA 30 year fixed rate mortgage:

-

One of the features of this type of loan is their fixed rate of interest. Irrespective of prevailing economic conditions and the rise in interest rates, you don’t have to worry about paying fluctuating rates of interest.

-

The FHA 30 year fixed rate mortgage option highlights the importance of securing a mortgage for individuals with limited savings. That is the reason for their lower down payment requirements.

-

Another attractive point is their lenient credit score requirements. So, if you are a borrower with credit score challenges, going for this option could be desirable.

-

As mentioned above, these loans are insured by the Federal Housing Administration, reducing risks among lenders, and paving the way to get the most favorable terms.

-

These loans allow flexibility to borrowers in case they decide to sell their home. The new home buyer can take over the existing loan, sometimes at lower interest rates than current market rates.

-

Unlike other loan options, FHA 30 year fixed rate mortgages require the borrowers to pay an upfront premium (Mortgage Insurance Premium) so that the lender is protected if the borrower defaults. Yes, this is an added cost but it enables borrowers with lower down payments to access homeownership.

Top 3 factors influencing mortgage rates

Before analyzing the current rates and trends, let us primarily understand the factors that influence mortgage rates. It is important to understand the various economic influences and the Federal Reserve’s policies. Come let’s take a closer look at these key factors:

-

Federal Reserve Policies

The interest rates are highly influenced by the decisions and policies taken by the Federal Reserve. Likewise, during times of economic growth, the Fed may raise its rate of interest to deal with inflation. This potentially increases the cost of borrowing in the mortgage rates. In contrast to that, the rates might come down if the economy goes downwards. This is done to stimulate borrowing and spending.

-

Inflation

Inflation rides over the purchasing power of the currency, so if the rates are on the rise, lenders tend to demand higher interest rates on loans, including mortgages.

-

Employment situation

The rise in employment figures also influences the interest rates you receive. This is why, when more people are employed and make a good living, they tend to invest in homes. It directly increases the demand for mortgages, and the lenders set the rates high.

These factors are one of the top determinants of your mortgage rates, and their change in patterns results in your rate increase or decrease.

What is a Mortgage Insurance Premium?

If you are ready to buy a home that you like the most with the FHA 30 year fixed rate mortgage option, be prepared to pay the mortgage insurance premium. Let’s understand about them in brief:

-

A mortgage insurance premium helps lenders protect their terms from high-risk borrowers.

-

This system is in place to help individuals who would be able to pay only a minimum down payment amount with lower credit scores. They ensure that lenders are protected if the borrowers fail to close the mortgage.

-

While the MIP increases a borrower's monthly costs, it still allows them to access the benefits of the loan in spite of their credit scores being lower.

Data on 30 Year FHA mortgages

According to Freddie Mac, nearly 90% of homeowners have a fixed mortgage rate at 30-year mortgage.

-

83.1% of mortgage applicants applied for a 30-year mortgage

-

89.0% of home buyers applied for a 30-year mortgage

Pros and cons of 30-Year FHA Mortgage

It is time to analyze both sides of the coin to make better financial decisions! Let's compare the pros and cons of opting for a 30 year FHA mortgage in the current mortgage industry.

| Pros | Cons |

|---|---|

| 1) They offer the best down payment options for homebuyers who are in a budget crisis. | 1) On the other hand, they have mandatory mortgage interest payments leading to increased monthly payments. |

| 2) Despite interest hikes, they still offer competitive rates to buyers without any bias. | 2) As the loan term is stretched further to 30 years, borrowers end up paying more interest over time compared to shorter-term loans. |

| 3) They offer lenient terms when it comes to credit scores and past financial setbacks. | 3) In addition to these upfront payments, you are required to pay closing costs depending on the amount you would like to borrow. |

Mortgage rate predictions 2024

Keeping several factors in mind, including the economic, financial, and Federal Reserve factors, we have saved some time for you by researching the mortgage rate predictions 2024.

Some mortgage experts have conveyed that the debate of whether the rates will go down is still on. However, a senior economist for Morningstar has predicted that the Fed might downsize the rates in February.

But, continuous analysis of mortgage rate predictions 2024 has taught us that, irrespective of the situation every individual must be prepared to face the fluctuations. With the rise or fall of rates, homeowners must ensure that they have a proper arrangement made to tackle the interest rates.

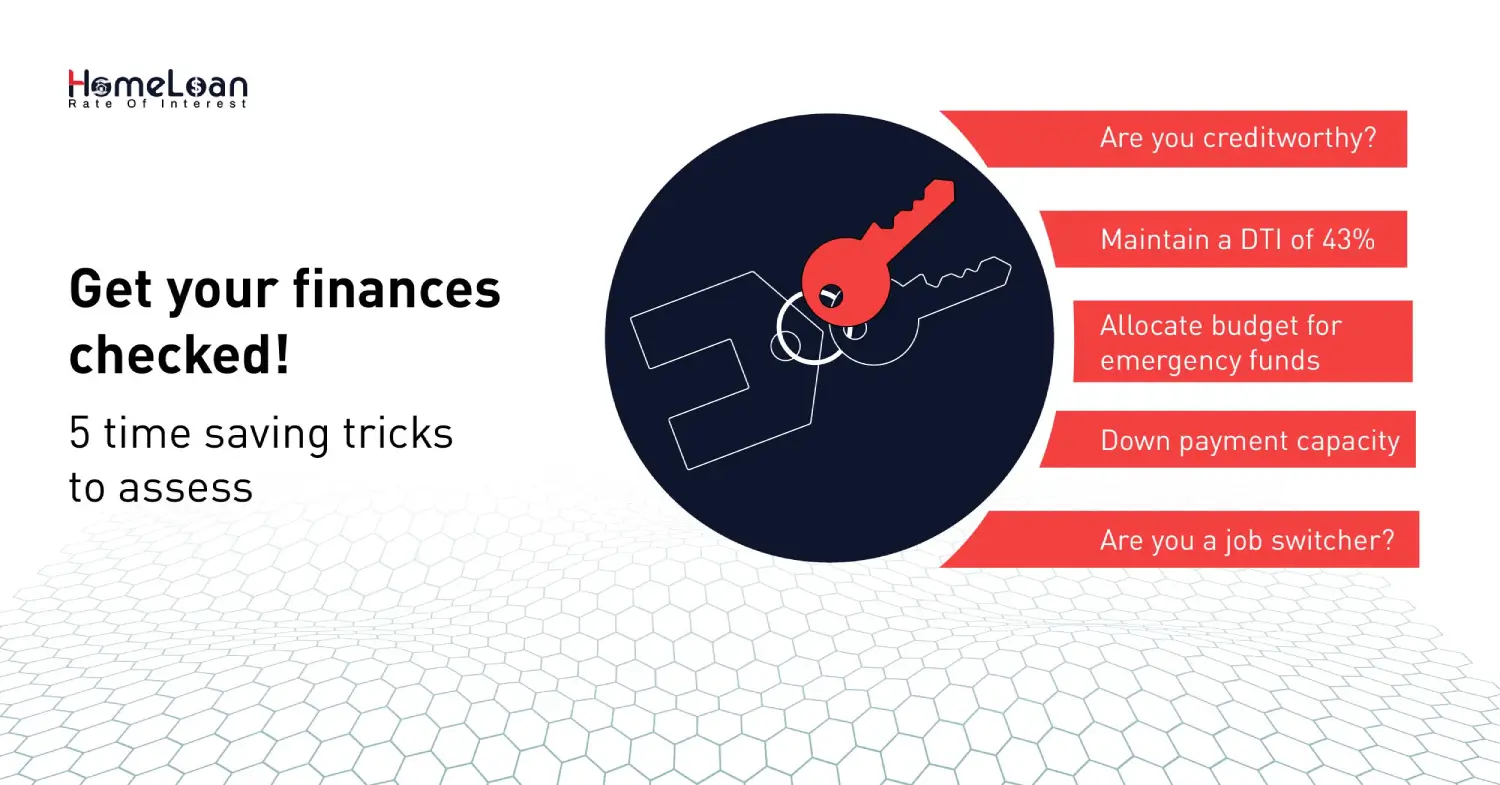

How to assess your financial situation?

If you want to know when is the good time to secure a 30 year FHA mortgage, that would be once you’re done with your financial situation assessment. Don’t worry! It is not complicated at all. It is a simple process of evaluating your financial history and anticipating your future financial requirements.

-

Creditworthiness

Let’s start with the most obvious step. Checking on your past credit performance helps lenders understand your creditworthiness. FHA loans are generally not strict when it comes to maintaining a great credit score, but it is advantageous to have a good credit score to prove your credibility.

-

Debt-to-income ratio

A DTI ratio determines how much debt you will be able to handle with the current income that you have. The required percentage that you’re required to maintain as part of your DTI is 43%. If you want to improve your DTI, you are supposed to pay current debt and pay off balances.

-

Budget and emergency funds

Creating a budget is as important as understanding the amount you would like to borrow. Make sure to allow space for monthly expenses. Understand if you can really make monthly mortgage payments even after meeting your monthly expenses. Maintaining funds for emergencies will help you tackle financial challenges without having to worry about taking out extra debt.

-

Savings with a down payment

Determine if you are willing to pay higher or lower down payments. Paying lesser down payments can help you secure a loan without much credit scores but opting for higher down payment can help lower monthly payments and reduce mortgage insurance costs.

-

Steady employment

You can attract better loan terms if you have a stable employment history. Your mortgage approval will be impacted if you have any gaps in your employment or frequent job changes.

As quoted by Napoleon Bonaparte, “Nothing is more difficult, and therefore more precious, than to be able to decide.” On that note, the decision making process to secure a 30 year FHA mortgage is not a breeze. Right from assessing your financial needs to choosing the right lender, if your decision leads to a minor mistake, it could have a major impact on your mortgage application.

As the mortgage rates continue to take their own course of a rollercoaster ride, staying informed about the current trends helps you ace your mortgage application process. If you have any other mortgage queries, get them addressed by HLRI’s mortgage advisors. Strategize your mortgage approach and be a homeowner at the right time.