- 31 May, 2023

Conventional Loans 101: A Comprehensive Guide for First-Time Homebuyers

Financing Your Future: Conventional Loans Simplified

Are you considering taking out a mortgage to buy your dream home? If so, you'll likely come across the term "conventional loan”. But what exactly is a conventional loan and how does it differ from other types of mortgages? In today’s blog post, we'll break down everything you need to know about conventional loans. From understanding conventional loans, how it works, who can qualify, pros and cons, to tips for borrowers, we've got you covered. So sit back, grab a cup of coffee, and get ready to become an expert on all things conventional loans!

A conventional loan is a type of mortgage that is not guaranteed by the government, unlike (Federal Housing Administration) FHA or (Veteran Affairs) VA loans. Instead, it is funded and insured by private lenders such as banks, credit unions, or other financial institutions. One of the main features of a conventional mortgage is its fixed interest rate. This means that you'll have a consistent monthly payment throughout the life of your loan. Additionally, conventional loans come with various term lengths ranging from 10 to 30 years.

Another important aspect to consider when applying for a conventional loan is the down payment requirement. While some government-backed mortgages allow borrowers to put as little as 3% down, most conventional lenders typically require at least 5% down.

It's worth noting that there are also two types of conventional mortgage loans: conforming and non-conforming. Conforming loans meet certain guidelines established by Fannie Mae and Freddie Mac while non-conforming do not. Ultimately, if you're looking for flexibility in terms of interest rates and repayment options, along with potentially lower fees compared to other types of mortgages, then a conventional loan may be an excellent choice for you!

Conventional loans are not backed by the government, unlike FHA or VA loans. Instead, private lenders offer them and they must conform to specific guidelines set forth by Fannie Mae and Freddie Mac. The loan amount is based on several factors such as credit score, income, debt-to-income ratio, job history and down payment. The higher your score and income with a lower DTI ratio could lead to better interest rates.

Unlike government-backed loans that have fixed interest rates for their entire term, conventional loans can come in two types: Fixed-Rate Mortgages (FRMs) which has the same rate throughout its life span of 15-30 years or Adjustable-Rate Mortgages (ARMs) which starts off with a low-interest rate but may vary depending on market conditions after a certain period of time.

Once you get pre-approved for a conventional mortgage loan from your lender of choice, you can start house hunting! If you find one that you like within the approved limit then you move ahead with purchasing it using funds provided by the bank or mortgage company.

Conventional loans are a popular option for borrowers who want to buy or refinance a home. But not everyone can qualify for these types of loans. Here's what you need to know about the eligibility requirements for conventional mortgage loans. Calculate your estimate today with HLRI!

Credit score is one of the most important factors in determining if you can qualify for a conventional loan. Generally, lenders prefer borrowers with good credit scores, which typically range from 680 to 740 or higher. A high credit score shows that you're responsible with your finances and have a history of paying bills on time.

Another factor that lenders consider when evaluating your application is your debt-to-income ratio (DTI). This is the percentage of your monthly income that goes towards paying off debts like mortgages, car loans, and credit cards. Lenders usually look for DTIs below 43%, although some may accept higher ratios depending on other factors such as credit score and down payment amount.

Down payment is also an important consideration when applying for a conventional loan. While there are programs available that allow low or even no down payments, many lenders require at least 5% to 20% down payment depending on the borrower’s financial profile. Borrowers should be able to provide proof of steady employment and sufficient income over time through pay stubs/ W2 statements, tax returns etc., demonstrating their ability to repay any loan taken out.

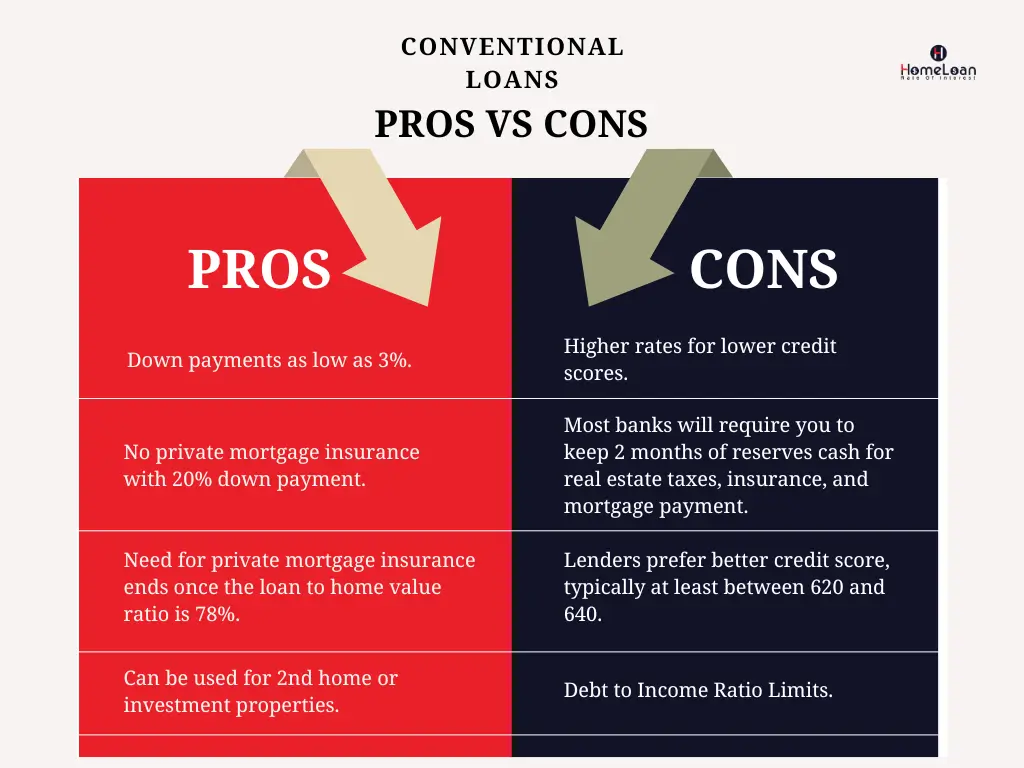

Conventional loans are a popular choice for borrowers who have good credit and can afford to put down a significant amount of money as a down payment. However, like any type of loan, there are advantages and disadvantages that borrowers should consider before applying.

One advantage of conventional loans is that they typically offer lower interest rates than other types of loans, such as FHA or VA loans. Additionally, conventional loans allow borrowers to finance larger amounts of money than government-backed loans.Another advantage is that private mortgage insurance (PMI) may be canceled once the borrower has paid off enough principal on their loan or if the home value increases significantly. This can save borrowers thousands of dollars over the life of their loan.

On the other hand, one major disadvantage of conventional loans is that they often require larger down payments compared to government-backed programs. This can make it difficult for some borrowers to qualify for a conventional loan if they do not have enough savings or equity in their current home. Additionally, unlike FHA and VA loans which have more lenient credit requirements, conventional lenders usually require higher credit scores from applicants in order to qualify.

While there are pros and cons to choosing a conventional loan over other options available on the market today - it ultimately depends on your individual financial situation and goals as a homeowner.

When it comes to borrowing a conventional loan, there are several tips that borrowers should keep in mind to ensure they make the most out of their experience. Here are some essential tips for borrowers:

-

Firstly, it is crucial to maintain a good credit score. A credit score plays a significant role in determining whether or not you will qualify for a loan and what interest rates you will be charged.

-

Secondly, before applying for a conventional loan, be sure to shop around and compare different lenders' offers. This way, you can find the best deal that suits your needs and budget.

-

Thirdly, always read through all the terms and conditions of the loan carefully. Make sure you understand everything before signing any documents.

-

Fourthly, try to save up as much as possible for your down payment. The more money you put down upfront, the less risk lenders consider taking on when approving your application.

By following these simple but effective tips while borrowing a conventional loan will help increase your chances of getting approved while keeping costs low.

To sum it up, conventional loans are a great option for those who have good credit and stable income. They offer a variety of benefits such as flexible repayment terms, low-interest rates, and no private mortgage insurance requirement.

If you're looking to buy a home or refinance your current mortgage with a conventional loan, be sure to do your research beforehand. Get quotes from multiple lenders and compare their offers carefully before making your final decision.

At Home Loan Rate of Interest, we understand there are some downsides to conventional loans like higher down payments and stricter eligibility criteria compared to other types of mortgages out there. We provide many advantages that can help borrowers achieve their dream of homeownership. So if you meet the requirements for a conventional loan comfortably then this could be an excellent choice worth considering!