- 14 Dec, 2023

A guide to choosing the perfect down payment amount for your home

Determine your conventional loan down payment amount

Found your home but still wondering what’s the right down payment to spend on your mortgage? Keep reading as we serve the deets to help you nail the perfect conventional loan down payment amount for your home.

Not just that, we will also break down the 6 different types of conventional loans that all home buyers should know. So, come let’s talk down payments!

Do down payments really matter?

Let’s find out!

A mortgage down payment is usually paid as upfront cash whenever a large purchase has been made. The remaining amount is paid with your mortgage.

Let’s consider an example - A 20% conventional loan down payment on a $400,000 home would be $80,000. This means that you will be paying a down payment of $80,000 and the principal loan amount would be $320,000.

The purpose of a down payment is to demonstrate the buyer’s financial capability and responsibility to lenders by ultimately reducing the amount that needs to be financed through a mortgage.

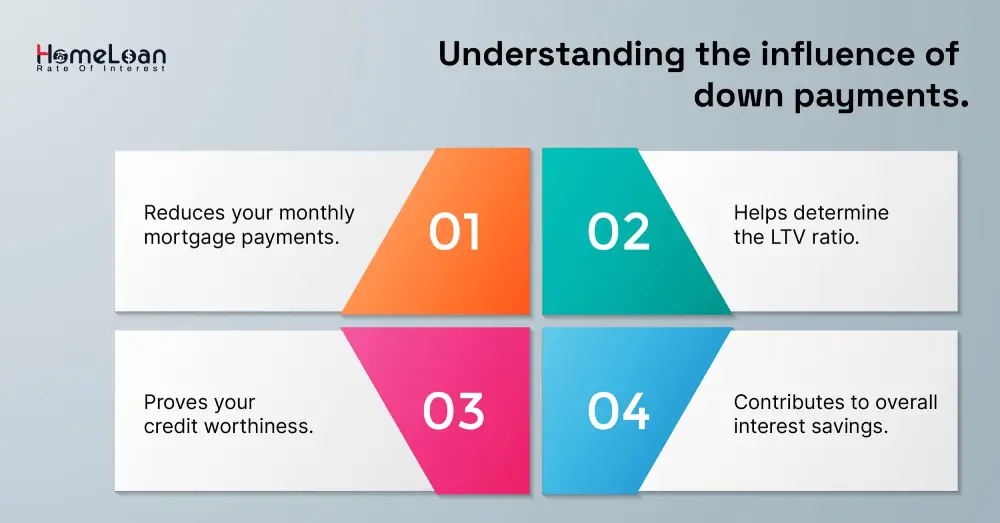

Benefits you get with a down payment

We all now know that a downpayment is a crucial element in the home-buying process as it shapes the terms of your mortgage.

From monthly payments to long-term interest rates, in this part of the blog, we will look at the different ways a downpayment can influence mortgage terms.

-

Helps lower monthly mortgage payments

-

One of the primary impacts of a conventional loan down payment is the potential to significantly lower your monthly mortgage payments. Here's how it works:

-

Smaller loan amounts

When you spend a good amount of down payment, the overall amount you need to pay is reduced.

So, with less money borrowed your monthly mortgage payments naturally become more manageable.

-

Loan to value ratio

The LTV ratio is assessed by the lenders to understand the risk they might be exposed to while underwriting a mortgage.

The 3 main factors that impact the LTV ratio are the amount of down payment, appraised property value, and sales price of the home.

If the ratio is higher than 80%, a borrower needs to get private mortgage insurance (PMI).

-

-

-

Reduces the overall interest rates

-

In addition to lowering your monthly payments, a substantial conventional loan down payment helps borrowers to pay reduced interest rates over the life of the mortgage.

-

A higher down payment enhances the borrower profile by showcasing a financial commitment as well as reduced risk for lenders.

-

And that’s how a substantial conventional down payment becomes a golden ticket to lower interest rates. It helps borrowers save thousands of dollars in the long run.

-

To make this a piece of cake, let’s look at the 5 proven tips to pick the right down payment payment.

5 proven tips to choose the perfect down payment amount

Well, buying a home is a big deal, and when it comes to making that dream a reality, figuring out the perfect down payment for conventional loan is like hitting a major crossroads. It’s one of the basic key moves that sets the tone for your entire home-buying process.

Gear for some tips to seize your perfect downpayment deal!

-

Get clarity on your financial situation

-

Before getting started with the conventional down payment requirements, make sure to check the overall financial situation. Evaluate your budget by analyzing your monthly income, expenses and savings.

-

Find out unwanted spending habits and try to cut them so you can spend well on your down payment. If you have any higher interest debts, pay them off so that you can manage your new monthly mortgage payments effectively.

-

-

Understand the basics of conventional loans

-

Many home buyers go for conventional loans as they require less paperwork and can be obtained faster than government-insured loans. However, they still have specific down payment requirements.

-

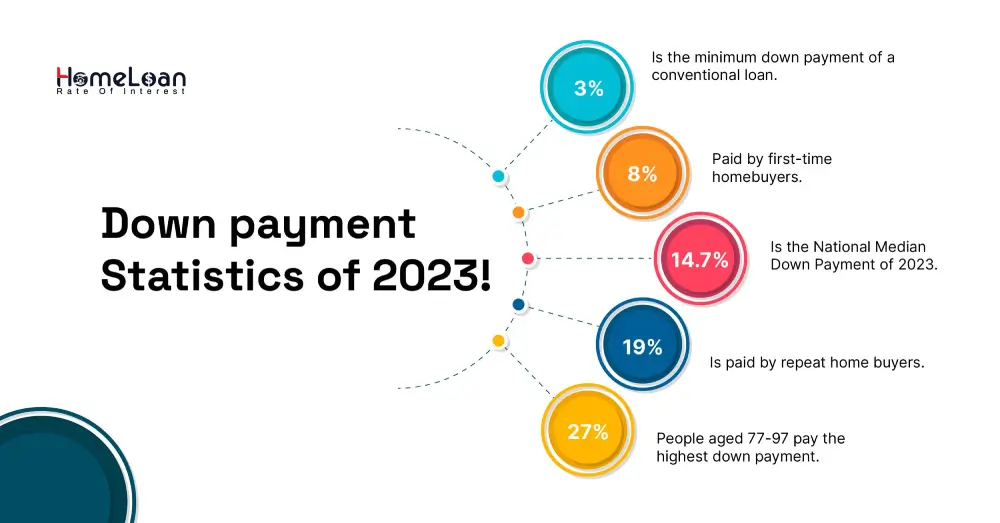

➙ Down payment - 20% of down payment is the standard for conventional loans. However, if you’re purchasing a loan for a primary residence, lenders accept down payment as small as 3 to 5%.

-

➙ Credit score - Lenders require a minimum credit score of 620 in order to get a better interest rate and terms.

-

➙ Debt-to-income ratio - Lenders mostly don’t want the DTI ratio to exceed 43% to 45%. So, make sure to maintain the same.

-

➙ Private mortgage insurance - If the down payment paid is less than 20%, borrowers need to pay an additional fee which is the PMI.

-

➙ Loan size - Conventional loans are mostly conforming, meaning they have certain limits based on the property’s location as they conform to Federal Housing Finance Agency (FHFA) limits.

Some of the basic conventional down payment requirements include:

-

-

Consider your affordability

-

Choosing a down payment isn't just about numbers, it's about your comfort and future financial well-being. So you need to determine a down payment amount that aligns with your monthly budget.

-

You need to be able to manage monthly mortgage payments, property taxes and insurance all at the same time. Create a source of emergency funds to allocate funds for uncertain times.

-

-

Find out down payment assistance programs

Why let go of various assistance programs that are meant to make your life easier?

Mortgage experts at Home Loan Rate of Interest will handhold you right from researching your state’s assistance programs till the end of application process making it easier for you to become eligible.

-

Did you know that there are 2500 programs available from state and local governments, as well as private and charity lenders to help borrowers meet their down payment requirements?

-

To qualify for the government assistance programs, borrowers must meet the lender’s income and credit requirements along with the DPA program guidelines.

-

-

Stay informed

-

Keep monitoring all your real estate market conditions and anticipating any potential fluctuations in your home values. Understand how the loan-to-value ratio influences down payment requirements.

-

Gauge the risk and financial implications of different down payment scenarios so that you can align your down payment strategy with long-term financial objectives.

-

-

Negotiate down payment terms

-

If you think you’re highly creditworthy then you can use it during negotiations and showcase your financial responsibility to secure favorable down payment terms.

-

Let your lenders know how a larger down payment impacts your monthly finances and negotiate for lower rates or reduced closing costs.

-

If you’re ready to utilize the above tips, get ready to learn about the 6 types of conventional loans that help you save on down payments, while allowing you to choose one loan type that best aligns with your unique financial circumstances.

6 types of conventional loans

Conventional loans are one of the popular options in the American mortgage market as they can be used to finance a range of properties and have limited restrictions compared to government-backed loans.

This makes conventional loans an appealing option for all borrowers who meet all approval standards. So if you’re planning to go for a conventional loan, buckle up and get ready to understand the top 6 types of conventional loans:

-

Conforming conventional loans

If the total loan amount you’re looking for is less than the maximum loan limits set by the Federal Housing Financial Agency, it’s called a conforming loan.

These conventional loan limits are set based on the current housing market conditions and property values.

So, if you’re going for a conforming conventional loan, make sure that the home you chose falls below the FHFA’s defined limits.

-

Fixed rate conventional loans

This is one of the widely used conventional loan types as interest rates are fixed and stay the same throughout the mortgage term. Many home-buyers opt for 30-year fixed rate loans as they come with affordable monthly payments.

-

Non conforming conventional loans

If your home’s purchase price is more than the FHFA loan limits or uses any other form of underwriting standard that is different from those set by Fannie Mae and Freddie Mac, it is referred to as a nonconforming loan.

So the alternate option could be going for a Jumbo Loan where the loan amount exceeds $484,350 in most U.S. counties.

Since the lenders of these loans are dealing with larger loan amounts, they might have stringent loan requirements and interest rates might differ compared to conforming loans.

-

Adjustable rate loans

The rate of interest in this type of conventional loan can go up or down depending upon the market conditions.

They are also known as hybrid ARMs, where the rates can be adjusted on an annual basis prior to the fixed rate period of 3, 5, 7 or 10 years based on the borrower’s financial background.

-

Low down payment loans

The standard conventional loan down payment was 20% but, today they have become more flexible.

Borrowers are now allowed to make as low as 3% to 5% down payment. With low conventional down payment loans, you can reach homeownership quicker.

But, the interest rate and monthly mortgage payment can be higher when you opt for low down payment loans.

-

Conventional rehab loans

These types of conventional mortgages are mostly used while buying a fixer-upper loan. They offer financing options to aid the move-in and renovation process.

With this loan in place, you need not be concerned about paying the additional cost of home repairs and upgrades. There is no need to get another loan, especially for home improvements.

Ready to make your smart move?

Choosing the right down payment requires careful consideration of personal financial situation. Affordable choices for some borrowers could be an expensive option for others.

So a perfect downpayment is one that aligns with your financial situation, goals, and the specific property you aspire to call home. It is always best to keep monitoring the conventional loan trends to make informed decisions.

If you’re still not sure about the conventional loan down payment, head over to our blogs to gain detailed insights about conventional loans.