- 26 Sep, 2023

When to Refinance Your Mobile Home: A Step-by-Step Guide

7 steps on how to buy a mobile home with refinancing

Whether you’re a young home buyer or you’re looking for pocket-friendly homeownership options, a Mobile Home is an appealing alternative to check out. Many homeowners achieve their dreams with the help of renting or refinancing their mobile homes. These mobile homes are not just affordable but highly easy to maintain. When it comes to homeownership in 2023, it is a challenging goal to achieve for many individuals.

Due to accelerating costs in mortgage interest rates, increased demand in the housing market, and inflation in the global economy, buying a house has become a stressful aspect for many residents in the United States. Despite these shortcomings, getting a place to call your own is possible with a mobile home.

If you’re an existing mobile homeowner, you know the pros! If you would like to improve your mobile home or use the equity built into your mobile home, a refinance could be a great option to use your funds efficiently. The time to refinance is something that we need to think about.

“If you haven’t found it yet, keep looking. Don’t settle. As with all matters of the heart, you’ll know when you find it.”

- Steve Jobs

In this blog, we will go through a step-by-step guide on when you can refinance your home and cover some of the tips that you can use to buy a mobile home and save on huge expenses like down payments and hefty interest rates. Come let’s get started!

What is the craze about mobile homes?

Before getting started with the available refinancing options, let us get an in-depth understanding of how mobile home ownership works. The term mobile home is a semi-permanent arrangement and can be moved from one place to another due to an individual’s personal or financial reasons. Many people call a mobile home a house trailer or a trailer home. It has got several nicknames. It is also called ‘manufactured homes’ at times.

Home Loan Fact!

21.2 million people in the U.S. live in a manufactured or mobile home. Around 85% of people are satisfied with their mobile or manufactured home.

3 practical features of mobile homes

-

The main difference between a mobile home and a manufactured home is the date of construction. HUD defines mobile homes as ones constructed before June 15 1976 and manufactured homes built after that date. However, they have the same setup and arrangement.

-

These homes are built in factories and can be transported to different locations. You can usually find mobile homes on private lands or by streams or rivers.

-

Compared to traditional ground-built homes, mobile homes are highly cost-effective to purchase and maintain. You get to personalize your home however you want and enjoy the benefits of homeownership easier, unlike traditional homeownership.

Why should you consider refinancing your mobile home?

If you’re an existing homeowner and want to secure more favorable terms with your mobile home loan, refinancing could be your best bet. It is the process of replacing your current mobile home loan with a new one with more favorable terms, probably lowering your interest rates or reducing the term of repayment. Below are some of the compelling reasons to consider refinancing your mobile home loan:

-

Lower monthly payments

One of the common reasons why many individuals in the U.S. choose to refinance is to secure a lower rate of interest that can ultimately reduce the monthly mortgage payments. Lower monthly payments can help allocate funds for any other expenses that you may incur on a monthly basis.

-

Reduced loan term

If you are in a better financial position currently than you were when you initially purchased your mobile home, you can consider refinancing as it will reduce your loan term. This means that you can pay off the loan quicker and save money for other expenses and investments in the future.

-

Access equity

As time passes and the economy grows, the value of your mobile home loan will simultaneously go up. With the help of refinancing, you can get more out of your mobile home by tapping into the equity. This enables you to access cash for various purposes such as home improvements and debt consolidation.

-

Debt consolidation

If you have high-interest debts from other sources, refinancing your mobile can be the ideal solution to get your bothering debts consolidated. It helps you to manage your finances better.

4 ways to assess your current mobile home loan.

In order to get into refinancing, you need to know how to assess your existing mobile home to make better decisions about your refinancing application. Here’s how you can go about it:

-

Review loan terms

Pull out your existing home loan papers and review your terms and conditions, interest rates, loan duration, and monthly payment values. Gather all the relevant documents needed with respect to your loan agreement.

-

Understand your interest rates

Pay attention to the interest rates you pay on your current mobile home loan so that you are aware of the current market rates. This proves to be beneficial to you especially when the market rates are higher. Once you understand the rates and stay updated, you will know the right time to refinance and get your interest rates lowered.

-

Evaluate monthly payments

Analyze your current financial situation. If your current monthly mortgage payments are draining your wallets, then it is the right time to refinance.

-

Calculate remaining balance

By determining the remaining balance on your mobile home loan, you can understand how much you need to refinance and whether you have sufficient equity in your home. If you have a higher portion remaining in your balance, refinancing could be considered.

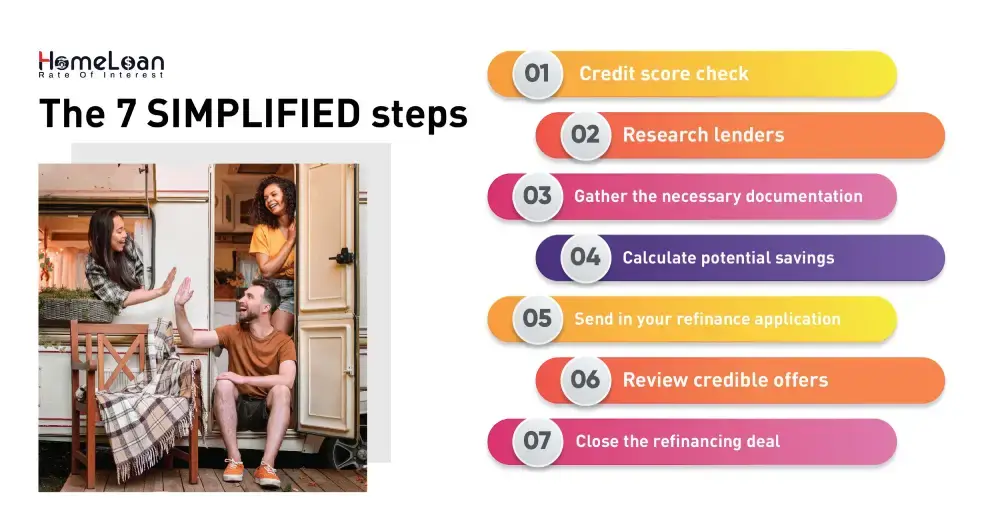

The 7-step refinancing process

Now that we have a fair understanding of how mobile home loans and homeownership work, let’s break down the steps for you to get started with the refinancing process without any hassles.

Step 1: Credit score check

Before you step into the refinancing process, it is highly recommended to get your credit scores checked and understand your creditworthiness. Your credit scores are carefully assessed to check your credit history and your ability to manage future credit payments. After a credit score assessment, if you still have your credit scores low, you need to try and improve them.

Your credit scores can range anywhere from 300 to 850. A higher score, helps you get better loan terms and qualify for a reduced interest rate. If not, take steps to improve your credit score by paying off outstanding balances and making timely payments.

Step 2: Research lenders

Depending on your location, lender terms and requirements change. Spend quality time researching lenders so that you can get your mobile home loan refinanced from a reputable lender. Here are a few things to consider while looking for lenders:

-

Look for lenders with reliable reviews and real-time testimonials from other borrowers. Check their credentials and consult with your close friends who have prior experience in getting a refinance loan.

-

Compare interest rates from multiple lenders to make sure you’re getting the best deals as lowering your interest rates can lead to substantial savings.

-

In addition to this, look for application fees and closing costs. These additional costs differ from one lender to another. Some lenders might be lenient and offer zero application fee offers if you have a strong financial profile.

Step 3: Gather the necessary documentation

To ease your refinance process, ensure that you grab all the necessary documents needed to start your refinance process. Doing this at the last moment can result in missing a few important documents that will have a bad impact on your refinance application. Some of the common documents that are essential include:

-

Proof of income (pay stubs, tax returns, or bank statements)

-

Proof of homeowners insurance

-

Your current mobile home loan statement

-

Mobile home title and registration

-

Identification documents (driver's license, social security number, etc.)

If you aim to secure favorable loan terms and fasten the refinance application process, get the essential documents ready.

Step 4: Calculate potential savings

Once you’re done with your lender research and document gathering, the next step would be calculating potential savings that you can achieve with the help of refinancing. Online tools and calculators can help you estimate interest savings, and monthly payments after your refinance application has been approved. If you want to save big with a refinance application, you can make use of these free resources to save and reduce your monthly payments.

Step 5: Send in your refinance application

Once you’re confident with your research, go ahead and send in your applications to be processed. The application process involves you providing the financial information, getting a credit check authorization, and finally submitting your loan application with your documents to the lender.

During this stage, you need to be prepared to answer questions regarding your employment history, income, and expense status. Once your application has been submitted, your lender will completely assess and check the confidentiality status to determine whether you qualify for the refinancing.

Step 6: Review credible offers

After the submission of your refinance application, you will start receiving offers from lenders. Take time to review these offers by paying attention to the interest rates, loan terms, closing costs and fees, and monthly payment amounts. Reviewing and comparing offers is crucial to finding the best refinancing deals.

Step 7: Close the refinancing deal

Once you have finalized your refinancing offer that suits your needs, it is time to move ahead and close the deal. Here you sign the new loan agreement, pay the closing costs and fees involved, and finalize the refinance process.

Make sure that you are careful and in sound mind while you’re finalizing your refinance application. It is highly important that you review the revised terms and interest rates. Once the deal is finalized your mobile home loan will be revised and replaced with a newer loan.

New home buyer? Here’s how to buy a mobile home

If you are living in a mobile home by paying monthly rent, you still have a chance to become a homeowner in the near future. Your mobile home rent is accumulated and used as equity to purchase the same home you lived paying monthly rent. In a mobile home rent agreement, you get to live in the home you want to buy in the future.

As a new home buyer, you know what your future home will look like, and it helps you make arrangements for your home in advance. Mobile home rent system offers flexibility to achieve homeownership goals.

Choosing a refinance option to revise your mobile home loan terms is the best option to consider when the rates are higher and you are unable to handle the pressure of making higher payments. However, if you are a newbie in the home buying process, we advise you to look for flexible mobile home buying or renting options as per your financial needs.

The current market conditions have a higher potential to impact your refinancing decisions, and if you’re still wondering how to buy a mobile home, head over to our blogs where we have created a series of information on how to get started with rent to own mobile homes.