- 28 Nov, 2023

Which is better to pay off first? 401k loan or HELOC

How does fixed rate HELOC work? Learn & get your estimate

With many financing options available for debt, decisions about repayment are crucial to consider. People tend to forget about repayment benefits while evaluating ways to access cash.

The decision of choosing between paying off a 401(k) loan or tackling a Fixed Rate HELOC is quite a challenge. In this blog, we will learn which is better to pay off first. Get bonus tips on how you can strategize your repayment plan.

What is a HELOC with fixed rate?

A home equity line of credit is one of the most opted financial tools used for debt consolidation. It is a line of credit based on your home equity and usually comes with variable interest rates.

-

There are two types of HELOCs, variable rate and HELOC fixed rate. The former option is issued by most lenders and the latter is hard to find as not all lenders offer fixed heloc rate.

-

HELOC is a revolving line of credit and the borrower is approved for a specific credit limit based on his/her home equity. Based on this limit, he/she can borrow against the limit and pay it back as per the repayment terms.

-

Borrowers can access funds only during the draw period which is between 5 to 10 years, followed by a repayment period.

-

When borrowers opt for a fixed rate HELOC, their homes act as collateral. So, if they fail to repay the loan, there are chances of foreclosure.

Get a quick HELOC estimate and get through the application process in just 3 steps.

Uses of 401(k) loan

A 401(k) loan involves borrowing from your retirement savings, specifically your employer-sponsored 401(k) account. It has tax advantages for the employee and can prove to act as a form of savings for the employee in the long run.

Here's a closer look at how 401(k) loans operate:

-

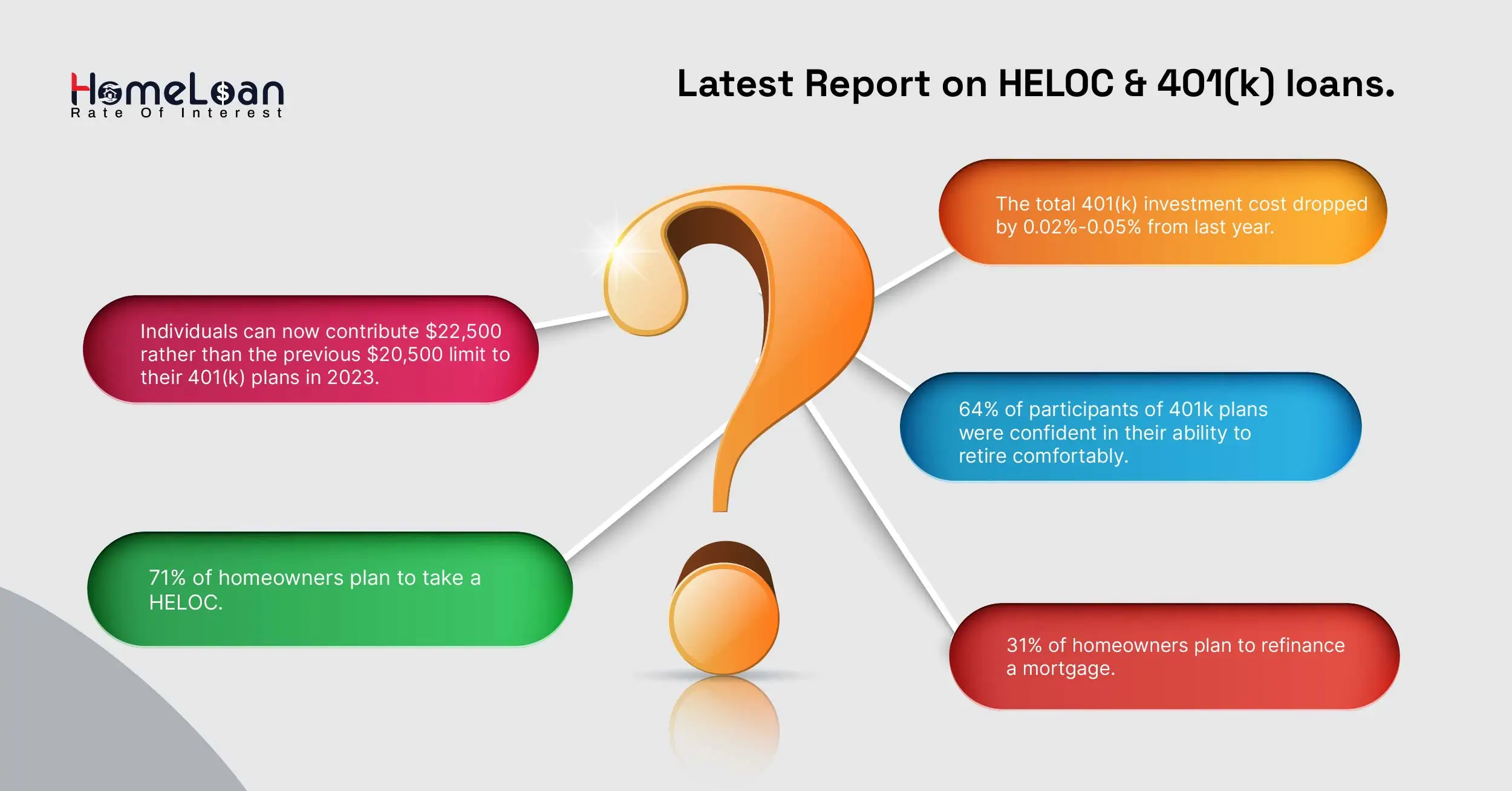

It is named after a section of the U.S. IRC - Internal Revenue Code and it sets the limits on how much can be borrowed from the 401(k) account.

-

When you take out a 401(k) loan, you can borrow up to 50% of your vested account balance that you own which is not more than $50,000.

-

The amount you can borrow depends on the rules established by the employer and the specific retirement plan. The repayment period of 401(k) loans is usually five years.

Pros and cons of Fixed rate HELOC

As a homeowner, getting a heloc with fixed rate might sound like the best option to access cash for debt consolidation or home remodels. However, when we are loaded with options it is best to choose after comparing both the pros and cons of fixed rate HELOC.

| Pros | Cons |

|---|---|

| 1) They offer flexibility and pave the way for better financial management as the rates are fixed and not variable. | 1) Similar to a home equity loan, a fixed Rate HELOC is secured by your property. So, failing to repay can lead to a major loss. |

| 2) You get to choose how the funds are being used by allocating the borrowed amount as needed. | 2) Since the amount borrowed is based on the total equity in your home, your borrowing capacity might go down if your home's value depreciates. |

| 3) No need to pay additional fees whenever the cash is being withdrawn. | 3) When you lock in the rates for HELOC, your lender might charge for it and there may be more penalties. |

After assessing the pros and cons of fixed rate HELOC, understand your unique financial circumstances, risk tolerance, and long-term objectives.

Pros and cons of 401(k) loans

Individuals who are in immediate need of financial assistance can choose to access funds from a 401(k) account. It is important to check with the employer if a 401(k) loan is feasible.

No matter how urgent the situation is, going blind with an option is not advisable. Let’s see the possible advantages and disadvantages of 401(k) loans.

| Pros | Cons |

|---|---|

| 1) Unlike fixed rate HELOC, 401(k) loans don’t require a credit check, making it easier for individuals with less-than-perfect credit. | 1) Borrowing funds from 401(k) loans results in a temporary reduction in your retirement savings. |

| 2) The 401 k loan interest rate paid goes back to your retirement account on a post-tax basis. | 2) In case of a job change, the borrower might face a due in their outstanding balance which might lead to a loan default if it can’t be repaid. |

| 3) The process is not tedious at all when compared to fixed rate HELOC as quick access is crucial when individuals want to access funds in urgency. | 3) There will be certain limits on the borrowing amount set by the IRS, making it a less ideal choice for larger financial needs. |

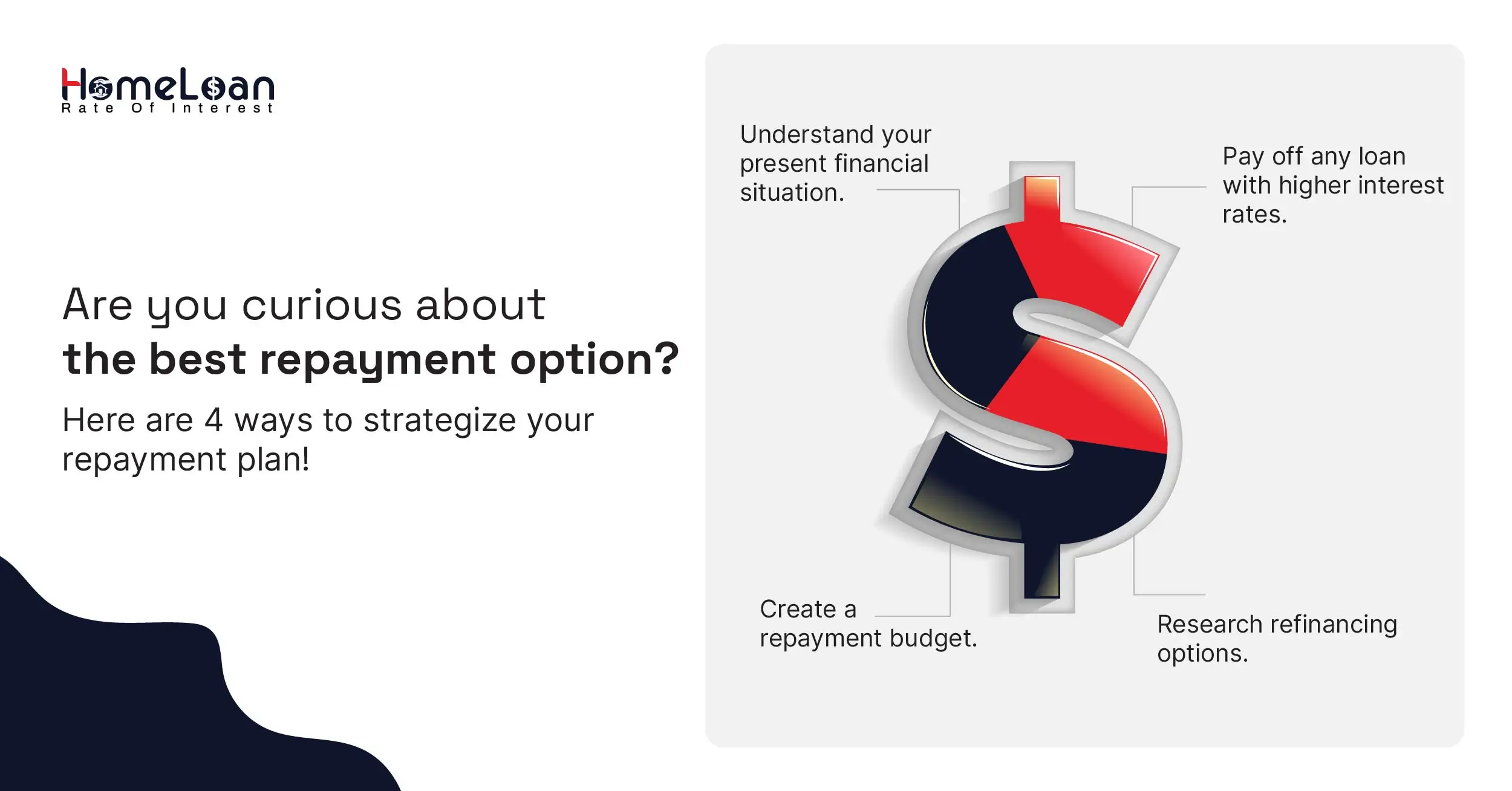

4 tips to strategize your repayment plan

As Benjamin Franklin rightly said - "Rather go to bed without dinner than to rise in debt." Repayment of debt must be given utmost importance as accumulated debt leads to stress and a weak financial portfolio.

Effective debt repayment involves careful planning and strategic decision-making. Consider the following steps to carefully plan your repayment:

Assessment of personal finances

Have a clear understanding of your income, expenses, overall debt, assets, and liabilities. This comprehensive assessment forms the foundation for informed decision-making.

Prioritize your high-interest debts

Borrowers might have a debt mix of high and low-interest debts. Prioritize and pay off all the high-interest debts so that you can save on significant costs over time.

Make sure you save funds for these high-interest funds rather than making unnecessary expenditures.

Look for refinancing options

Research the available opportunities to refinance by renegotiating or locking in more favorable terms to reduce the overall financial burden. Assess the potential benefits of securing lower interest rates through refinancing.

Allocate repayment budget

It would be great if you could create a well-structured repayment budget by allocating a portion of your income to prevent future financial strain.

You can make use of an online budget tracker and identify areas where you can cut back on discretionary spending to allocate more funds toward debt repayment.

Understanding 401k interest rate

This is a unique type of loan, wherein the 401k loan rates paid go back into your own retirement account rather than your lender’s account.

The interest rate of 401k loans are much lower than other types of loans and they are 1% or 2% more than the prime interest rates. For instance, if the prime interest rate is 7%, the 401k interest rate will be 8%.

Which is better to pay off first?

Do you want to know which type of loan offers a better repayment option? Is it a 401k loan or a HELOC?

The decision on which to pay off first depends on various factors, including your financial goals, risk tolerance, and the terms of each loan. Here are some factors you should consider before deciding:

Interest rate

Compare the HELOC and 401k interest rates. If one has a higher interest rate, it may make sense to prioritize that debt first to minimize overall interest payments.

Tax implications

Consider the tax implications of each loan. While 401(k) loan repayments are not taxed, interest paid on a Fixed Rate HELOC may be deductible. Consult a tax professional or a mortgage professional to understand the specific impact on your situation.

Review Repayment Terms

Examine the repayment terms of both loans. If one has more favorable terms, such as a longer repayment period or lower monthly payments, it may influence your decision.

Risk tolerance

Evaluate your risk tolerance based on your personal financial situation. If the potential risks associated with one type of loan make you uncomfortable, it might be prudent to prioritize repayment of that debt.

Therefore, it is important to think from your own shoes. Whether you choose to repay the 401k loan first or the HELOC, make sure to consult with a mortgage professional who can guide you through the repayment process.

Impact of credit scores on 401k interest rates & HELOCs

It is not a surprise that good credit scores result in lower interest rates. Borrowers with a higher credit score can show a record of consistent and timely debt repayment.

-

As there is no credit check on 401k loans, HELOCs require borrowers to maintain a decent credit score.

-

Lenders assess the creditworthiness of the borrowers to measure how they pay back the loans and deal with credit cards.

-

Gain a comprehensive understanding of credit scores, including the primary credit scoring models like FICO used by lenders.

-

Good credit score always proves to be favorable for both the lenders and borrowers as they are observed as less risky.

As we wrap up the blog, let’s run through the essential points to help you make a better decision.

Recognize that mortgage markets evolve, and staying informed can be your greatest savior. Whether it's changes in interest rates, market dynamics, or personal financial goals, ongoing awareness about the mortgage market is key.

Consider asking for help as it only helps you handle complex decisions and optimize your financial journey.

Finally, make sure that you maintain healthy financial habits so that your creditworthiness is never questioned.