- 09 Jan, 2024

A Step-by-Step Guide to Minimize USDA Closing Costs in Florida

Who pays USDA closing costs in Florida for a house?

Are you considering a USDA loan? Awesome choice. There are ways you can include the closing costs right into your USDA loan. Stick with us till the end of this blog, as we share the tips and steps to lower your USDA loan closing costs in Florida.

Closing costs in Florida

Closing costs can be one of the barriers to you, especially if you don’t have enough cash saved to meet the ongoing homeownership expenses. In Florida, the closing costs are slightly higher than the national average of 1.81%.

But, there is a way to tackle and trim down your costs so you don’t have to worry about spending more than what’s necessary. Scroll down to know how.

Step-by-step guide to minimize USDA closing costs

There’s no way to exclude the closing costs entirely from your mortgage. But, you have control over the USDA loan closing costs as they are not fixed and same for all homebuyers.

They depend on three main factors – The total price of your home, its location, and if you’re buying a new home or refinancing it.

Here are the potential ways for you to save money on closing costs in Florida:

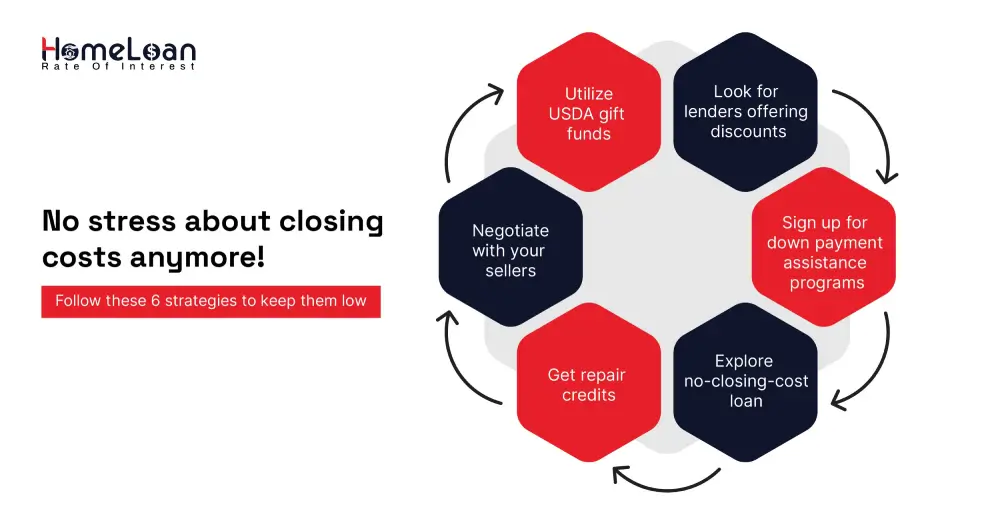

Step 1) Utilize discount opportunities

-

Look for mortgage lenders who offer discounts. You can apply with a lender who either doesn't charge an origination fee or is willing to cut you a deal.

-

If you're already a customer at a bank where you're getting your mortgage, don't hesitate to ask for a discount or even a fee waiver. Sometimes, it pays to be a loyal customer.

Step 2) Check out down payment assistance programs

-

If you’re a first-time homebuyer, don’t leave this unnoticed. Explore down payment and home buyer assistance programs in Florida.

-

They can offer you a dual benefit. They help you with down payments as well as cover a portion of your closing costs.

-

But, you don’t have to stress about down payments! Yes, that’s right. Get your quote from Home Loan Rate of Interest and say goodbye to hefty down payments.

Step 3) Get a no-closing-cost loan

-

Firstly, don’t get influenced by the name. It doesn’t mean that your closing costs are completely off the hook. What it does mean is that you have options.

-

You can either finance the closing costs along with your mortgage or opt for a slightly higher interest rate.

-

It's a bit of a trade-off, but it can be a strategic move if you prefer to manage your cash flow differently.

Step 4) Look for repair credits

-

If your home inspection reveals issues you'd prefer to handle yourself, don't hesitate to negotiate with your lender.

-

Ask for a repair credit that can be applied to offset the USDA closing costs. It's a win-win situation that ensures you have the flexibility to address the issues on your terms.

Step 5) Know what your seller is paying

-

Sometimes, your seller can cover the closing costs too. They are known as seller concessions and include all the closing fees and home repairs.

-

Mortgage programs have certain rules on USDA home loan closing costs that can be covered by the seller. So, before you negotiate with your seller, make sure to check with your lender.

Step 6) Make use of USDA gift funds

-

USDA loans offer gift funds and you can use them to pay towards your closing costs. It means that the approved family and friends can provide you with cash gifts.

-

Apart from this, you can also use charitable donations and employer assistance as gift funds, but lenders will require you to submit a gift letter and other supporting documents as part of the loan.

Closing fees in Florida are a common part of the home-buying process, but these steps empower you to have more control over your USDA loan closing costs.

Remember, a little negotiation and research can go a long way in making those USDA closing costs a bit more manageable.

Visit Home Loan Rate of Interest and grab your USDA eligibility checklist.

Closing costs are not just a single expense. Nope, they're a whole package covering lender charges, appraisal fees, and a bunch of other third-party costs. that we will discuss in detail in the upcoming section.

Closing costs breakdown

Closing costs are necessary, yet they are still surprising to many homebuyers as they come in different ranges depending upon the loan type and amount you get.

They are additional fees that homebuyers are responsible for paying when they are in the final stages of closing their mortgage application.

Are you aiming to shrink those closing costs, the first thing to do is to understand what exactly makes them up. Why? Well, knowing the tiny details will give you an upper hand in predicting and organizing your finances ahead of time.

Here's a brief explanation of each fee included in closing costs in Florida

-

Application fee -Charged by the lender to process the loan application.

-

Credit check fee -The cost of checking the homebuyer's credit history to assess creditworthiness.

-

Origination Fee -Charged by the lender for processing the loan application, often expressed as a percentage of the loan amount.

-

Underwriting fee -They are paid by the borrowers to cover the lender’s overhead expenses for underwriting the mortgage by evaluating the risk and eligibility of the loan.

-

Appraisal fee -It is the expense associated with assessing the market value of the property.

-

Property survey fee -The cost of surveying the property to confirm its boundaries and characteristics.

-

Title search fee -This is the charge for researching public records to verify the property's ownership history.

-

Title insurance policy -Insurance that protects the buyer and lender against any potential title disputes.

-

Attorney fee -Legal fees for services provided by your attorney during the closing process.

-

Discount points -Fees paid to your lender at closing in exchange for securing a lower interest rate.

-

Transfer Tax -A tax imposed by the local government when the property changes ownership.

-

Recording Fee -The cost of recording the new property deed with the county.

There you go, these are some of the important components that collectively make up your closing costs in Florida, and the responsibility to pay can be negotiated between you and your seller.

How are the costs included in the USDA loan?

The USDA closing costs are not included in your mortgage by default. But, if you get the USDA single family guaranteed loan program, there is a unique feature that allows you to finance up to the appraised value.

This is a bit confusing, right?

To put it in simple words, when the appraised value of your home is more than the sales price, the USDA home loan closing costs will be included in your loan. These costs can be financed into the USDA loan:

-

Title charges, loan costs, recording, survey fees, etc.

-

Homeowner’s insurance premium, prepaid interest, and escrow accounts.

-

Eligible repairs that are to be completed after closing under the USDA escrow repair holdback feature.

So, if your appraised value is not more than the sales price, you might have to pay the USDA loan closing costs out of your pocket or negotiate with your sellers to pay.

Who pays closing costs in Florida?

With the closing costs being the highest in Florida, you will have to pay closing costs that range from 2% to 5% of the purchase price, and in Florida, the costs can go up as the housing market is highly expensive.

But, who is responsible for paying these costs? Do you bear the whole cost of closing fees in Florida?

Partly yes and no! Buyers are typically responsible for paying but in some cases, your sellers might agree to pay a portion. These are the list of costs your seller might incur if you negotiate with them:

-

Real estate commission

-

Title insurance

-

Transfer taxes

-

Property taxes

-

Document preparation fees

At the end of the day, paying closing costs is a shared responsibility. Brush up your negotiation skills and talk to your lenders about the closing costs. Have supportive documents to prove your side of the bargain and see how it goes.

Can you avoid paying closing costs?

We get it, the home buying journey is exciting and at the same time challenging because you need to deal with mortgages, hunt for houses, and arrange finances for down payments and closing costs like these.

So, to answer your question, you can’t avoid the closing costs but there are strategic moves that can help you manage the payment more effectively.

Closing costs are a reality, you can minimize the costs by negotiating with lenders and exploring local programs. Additionally, you can strategically time your closing so that you are equipped with enough money to meet these costs.

Remember, you have the power to control how much you pay toward the closing costs.With the right approach, you can turn this financial checkpoint into a manageable step while closing your application.

Happy house hunting! 🏡