- 10 Nov, 2023

8 Reasons Why Applications for FHA Loans Are Decreasing

Definition of FHA connection and the key facts

FHA loans are a strong preference for borrowers with damaged credit and those who have limited funds allocated for down payment.

Many first-time home buyers choose an FHA loan over other loan types as it has lenient requirements. However, the FHA loan is not suitable for all borrowers and that’s exactly what we’ll be discussing in today’s blog stating the 8 reasons why applications for FHA loans are decreasing.

FHA loans: How do they work and requirements

Federal Housing Administration loans are backed by the government and issued by an FHA-approved lender. FHA loans aim to make the borrower’s life easier by offering loans with lower interest rates and down payment.

They are entirely different from conventional mortgages and are specially designed to help low to moderate-income families attain home ownership.

However, they have certain requirements to ensure lender security in case of financial uncertainties for the borrower:

→ Mortgage Insurance

-

This insurance protects lenders from financial losses in case a borrower defaults on the loan.

-

Mortgage insurance premium not only acts as a safety net for lenders but also for borrowers because an absence of it would require borrowers to pay a higher premium amount.

-

There are 2 types of mortgage insurance premiums, an upfront payment and an additional annual payment, and the amount paid as premiums depends on the total loan amount.

-

The former comprises 1.75% of your FHA loan’s total value and you’re required to pay this percentage of your loan amount as an upfront payment before loan closing.

-

The latter, i.e. - the annual FHA MIP, varies based on your loan-to-value ratio. Mostly, you don’t have to worry about paying a bulk annual amount as lenders add the annual MIP to your monthly mortgage payment.

-

With the existence of mortgage insurance premiums, lenders are more willing to extend credit to borrowers who might not meet the strict criteria of a conventional loan.

-

→ Credit requirements

-

Mortgage insurance premiums could be a drawback for individuals who find it difficult to afford. That’s one of the reasons why lenders are becoming more approachable, by offering lenient credit requirements.

-

It doesn’t mean that they accept applications with completely bad credit scores, borrowers are expected to have a decent credit history.

-

Though the exact credit score requirements can vary, most lenders prefer a FICO credit score of at least 580. Those with lower credit scores may still be eligible but might face stricter mortgage terms and requirements.

-

Top 8 reasons why FHA applications are decreasing

Now that we know about FHA loans and their requirements, it is time to understand the reasons behind the fall in applications to make better home-buying decisions.

Let’s examine why people choose to go for FHA construction loans & what's causing this shift away from a popular loan program that has historically made homeownership more accessible for countless individuals!

Eligibility has become stricter

-

Recently, FHA has decided to make the eligibility a bit stricter than usual in an effort to reduce risk and protect taxpayers.

-

This has made the lenders inspect the financial backgrounds of borrowers with the intention of observing credit stability. This has led to major rejections for borrowers who fall under a 580 credit score.

-

Apart from credit requirements, new borrowers are also required to meet more stringent income criteria, and debt-to-income ratio requirements, which can be a barrier to entry for some.

-

Interest rates are rising

-

Interest rates play a major role in all types of loans. As the demand for FHA loans is higher, the rate of interest has not gone down yet.

-

Relatively, with the rise of interest rates, the cost of borrowing increases, making FHA loans less appealing.

-

This is one of the primary reasons why borrowers may seek other loan alternatives apart from FHA loans.

-

With recent inflation, interest rates have seen fluctuations, affecting the affordability of FHA loans.

-

Comparison with conventional loans

-

The direct competitors of FHA loans are conventional loans and they are neither insured nor backed by the government.

-

They are offered by private lenders and government-sponsored enterprises such as Fannie Mae and Freddie Mac.

-

The loans offered by private lenders need not be necessarily approved by the government but must meet federal, state, and local regulations.

-

A conventional loan is a great option for borrowers who have a strong credit history and a higher income profile.

-

The reason why FHA applicants are moving towards conventional loans is that their rate of interest is fixed throughout the loan term. As a result, potential homebuyers find it safer to opt for a conventional loan.

-

Economic factors

-

Economic conditions and downturns also have a significant impact on the demand for FHA loans.

-

People who preferred to take an FHA loan before inflation were relatively higher than individuals who took FHA loans post-inflation.

-

Additionally, inflation has also impacted the job market ultimately resulting in people losing their jobs. Due to this, people’s income decreases and homebuyers postpone their plans of buying a home and taking out a mortgage.

-

FHA construction loan

-

Many home buyers who find it difficult to purchase a home of their dreams due to supply shortages, decide to build a home as lenders accept a credit score starting from 500.

-

In recent times, this option didn’t seem to appeal to many homebuyers with lower credit scores as the down payment requirement was higher for all the credit scores below 580.

-

FHA construction loan is not a straightforward approach to home ownership and could be an added responsibility with potential complications in a construction project.

-

This potentially affects the overall demand for FHA loans making it a less desirable option for home buyers.

-

To meet the basic FHA construction loan requirements, borrowers must have a credit score of at least 500, and maintain a DTI ratio of no more than 43%.

-

Fluctuation in mortgage insurance premiums

-

As discussed above, mortgage insurance premiums (MIPs) are a critical component of FHA loans, as they protect lenders against borrower defaults.

-

There has been a hike in MIPs recently making it a less affordable loan for low to moderate-income families.

-

The higher premiums ultimately increase the overall cost of FHA loans and homebuyers don’t want to face these additional expenses and higher costs.

-

Other debt options

-

Other higher debts such as student loans have emerged as a barrier to applying for an FHA loan. This is because high levels of student debt can increase a borrower's debt-to-income ratio, making it challenging to qualify for an FHA loan.

-

Many potential buyers who are already burdened with student loans, find it difficult to meet the

FHA's eligibility criteria.

-

Lack of awareness

-

Certain early and elderly homebuyers don’t have much awareness of FHA loans and their uses.

-

This lack of awareness is a missed opportunity for those who could benefit from FHA loans but never explore them as an option.

-

If you would like to stay informed and updated about FHA and other loan types check out our blog page which consists of a series of useful mortgage information.

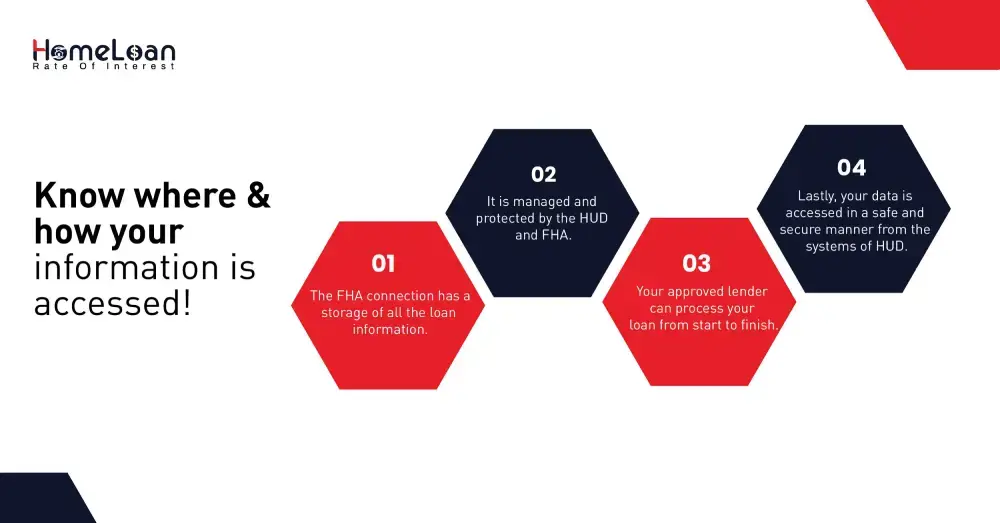

FHA connection system definition

FHA connection provides FHA-approved lenders and partners with a safe and secure platform to access the computer systems of the U.S. Department and Urban Development (HUD). It is an online platform entirely managed by the HUD and FHA.

FHA connection is a user-friendly system that is designed to streamline and facilitate the management and maintenance of FHA-insured loans, offering essential tools and resources for lenders, mortgagees, and other stakeholders involved in the FHA loan process.

4 Key facts about FHA connection

-

Provides the most secure access to borrower data while making it an accessible platform to a wide network of FHA-approved lenders.

-

By using FHA connection, lenders simplify the process of originating, underwriting, and servicing FHA-insured loans.

-

The FHA connection system offers a "Case Query" feature, enabling authorized users to retrieve detailed information about specific FHA loan cases. This tool is invaluable for tracking the status of loan applications and approvals.

All you need to do is enter the first three characters of the case number and you will have the entire case details displayed on the screen.

-

The platform proves to be a resource center for the lenders helping them navigate the loan process information effectively.

Now you know why there is a decrease in applications for FHA loans. While these challenges are evident, if you’re a homebuyer who is ready to face and overcome the situation, an FHA loan is still not a bad choice.

These factors such as eligibility criteria, rising interest rates, economic factors, and changes in mortgage insurance premiums are bound to change as the market trends fluctuate.

If you’re a first-time home buyer and want to strategize your FHA construction loan plan, get in touch with HLRI’s support team and get a swift response.