- 19 July, 2023

Home Equity Loan Vs HELOC: Finding Your Perfect Fit

Comparing Home Equity Loan and HELOC: Which is Right for You?

In today’s blog post, we'll delve into the comparison between a Home Equity Loan and a Home Equity Line of Credit (HELOC). By understanding the differences and benefits of each option, you'll be well informed to make the right choice for your unique needs. So, let's get started on finding the perfect fit for potential purchase of your home equity.

- Suze Orman

Home equity, in simple words, refers to the portion of your home that you truly own - the value you've built up over time by paying off your mortgage or through appreciation in the housing market. It's an asset that can be used to secure a loan, giving you access to funds for various purposes.

-

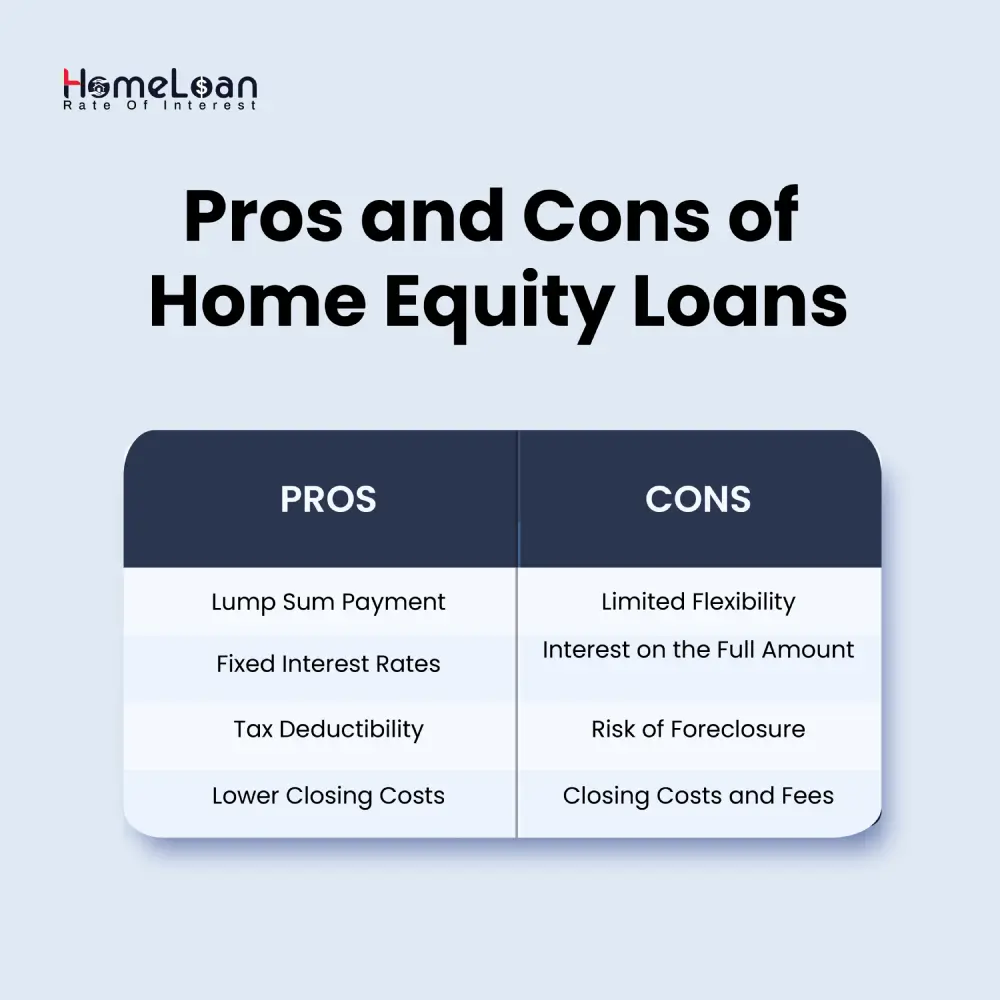

) Lump Sum Payment: A home equity loan provides you with a one-time lump sum payment, making it ideal for specific expenses like home renovations or consolidating high-interest debt.

-

) Fixed Interest Rates: With a home equity loan, you'll have the advantage of a fixed interest rate, providing stability and predictability in your monthly payments.

-

) Tax Deductibility: In many cases, the interest paid on a home equity loan is tax-deductible, potentially saving you money come tax time.

-

) Lower Closing Costs: Compared to other loan options, home equity loans typically involve lower closing costs, making it a more affordable choice.

-

) Limited Flexibility: Once you receive the lump sum, you won't be able to borrow more against your home equity loan without refinancing.

-

) Interest on the Full Amount: With a home equity loan, you pay interest on the entire loan amount, even if you don't use all the funds.

-

) Risk of Foreclosure: Defaulting on your home equity loan payments could put your home at risk of foreclosure, so responsible borrowing is crucial.

-

) Closing Costs and Fees: While home equity loans generally have lower closing costs, there may still be fees involved, so it's important to carefully consider the overall cost.

Now that we are aware of home equity loans, let’s take a look at what HELOC is. A Home Equity Line of Credit is another way to access your home equity. Unlike a home equity loan, a HELOC works more like a credit card, allowing you to borrow against your home equity up to a predetermined credit limit. You can borrow as much or as little as you need, when you need it, within the specified draw period.

Pros and cons of HELOC

-

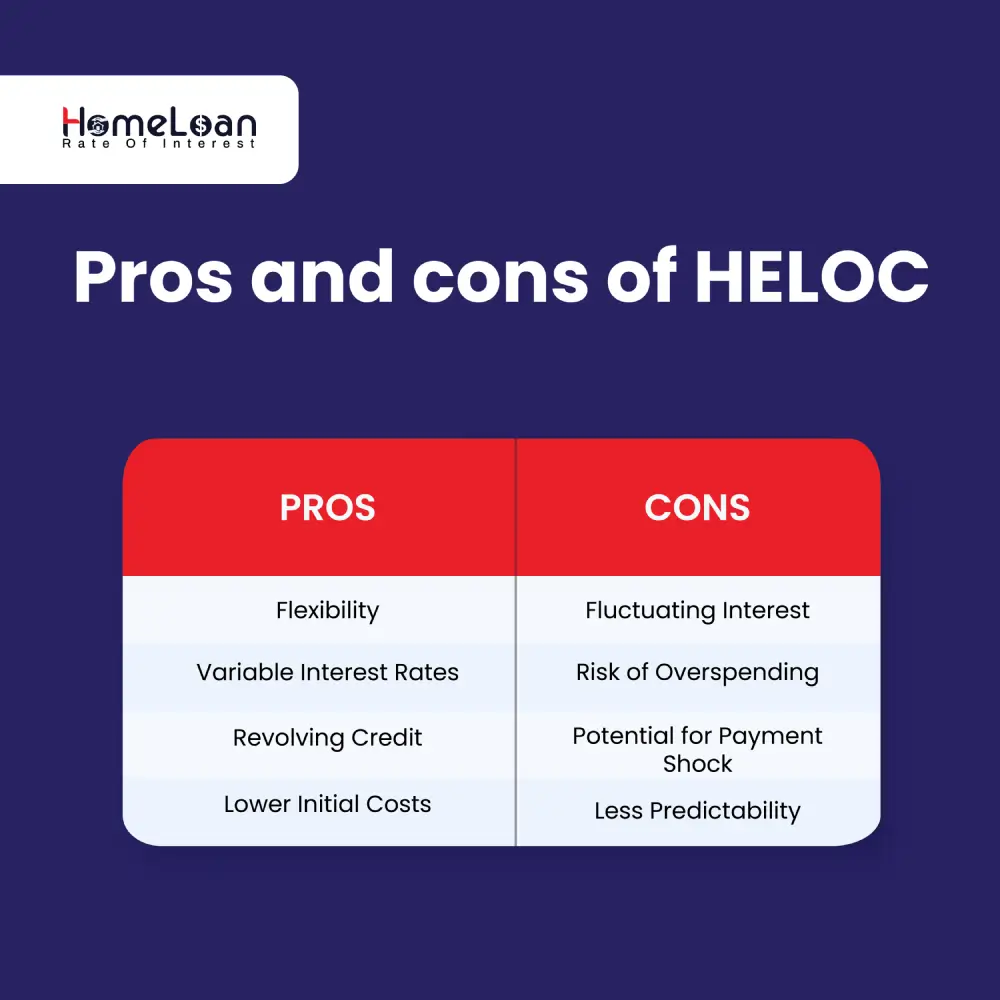

) Flexibility: A HELOC offers the flexibility to borrow only the amount you need, giving you control over your borrowing and repayment.

-

) Variable Interest Rates: HELOCs often come with variable interest rates, which can be advantageous if rates are currently low. It also means your payments may vary over time.

-

) Revolving Credit: Similar to a credit card, a HELOC allows you to borrow, repay, and borrow again during the draw period, giving you ongoing access to funds.

-

) Lower Initial Costs: HELOCs generally have lower initial costs, such as application fees and closing costs, making it an appealing option for those looking for cost-effective borrowing.

-

) Fluctuating Interest Rates: While variable interest rates can be advantageous, they also come with the risk of increasing rates over time, which could lead to higher monthly payments.

-

) Risk of Overspending: The flexibility of a HELOC can tempt you to overspend, so it's important to create a repayment plan and use the funds responsibly.

-

) Potential for Payment Shock: As the draw period ends and the repayment period begins, your payments may increase significantly, causing potential financial strain if not planned for.

-

) Less Predictability: Unlike a home equity loan, where you have a fixed payment schedule, a HELOC's variable interest rates and potential for payment changes mean less predictability in your budgeting.

The main difference between a home equity loan and a HELOC lies in how you access and repay the funds. While a home equity loan provides a lump sum payment with a fixed interest rate, a HELOC offers a revolving line of credit with a variable interest rate.

| Home Equity Loan | HELOC (Home Equity Line of Credit) | |

|---|---|---|

| Access to funds | Includes lump sum payment | Includes revolving line of credit |

| Interest Rate | Interest rate is fixed | Interest rate is variable |

| Repayment Structure | Repayment terms are fixed | Draw period followed by repayment terms |

| Flexibility | Limited flexibility | High flexibility |

| Usage | Ideal for one-time expenses or debt consolidation | Suitable for on-going or variable expenses |

| Interest Payments | Interest paid on the entire loan amount, even if not used in full | Interest paid only on the amount borrowed |

| Additional Borrowing | Requires financing for additional borrowing | Can borrow, repay and borrow again within the draw period |

| Payment Predictability | Fixed payment schedule | Potential payment fluctuations |

-

Choosing between a home equity loan and a HELOC depends on your financial goals, borrowing needs, and personal circumstances. If you have a specific one-time expense in mind or prefer the stability of fixed payments, a home equity loan may be the better option.

-

On the other hand, if you value flexibility, ongoing access to funds, and can handle potential payment fluctuations, a HELOC might suit you better. Always make sure to consider your financial objectives and consult with a trusted financial advisor to make an informed decision.

Ultimately, whether you opt for a home equity loan or a HELOC, it's crucial to understand your financial situation, set clear goals, and borrow responsibly. Educate yourself about the loan terms, interest rates, and potential risks involved. Don't hesitate to reach out to multiple lenders to compare offers and find the best place to obtain a HELOC or home equity loan that aligns with your needs and preferences.

By leveraging the power of your home equity wisely, you can unlock opportunities for home improvements, debt consolidation, education expenses, or any other dreams you may have.

So go forth, explore your options, and make the choice that empowers you to achieve your goals while maintaining your financial well-being. Your home equity can be a valuable tool in shaping the future you desire.