- 18 Dec, 2023

How Federal Reserve Rate Cuts Influence Home Buying Strategies in 2024

Will there be a drop in mortgage rates 2024? What to expect?

If you have tried to purchase a home in 2023, you might have noticed that mortgage rates were higher.

One of the main reasons for the increased mortgage prices would be frequent rate hikes by the Federal Reserve. But, the good news is that 2024 is anticipating a decrease in mortgage rates.

In this blog, we will break down the silence about the impact of inflation on your finances and analyze the trends in mortgage rates 2024.

Is inflation likely to lower mortgage rates in 2024?

Did you know that Americans owe $12.14 trillion on 84 million mortgages? That comes to an average of $144,593 per person with a mortgage on their credit report. Mortgages represent 70.2% of consumer debt in the U.S.!

Surprising right?

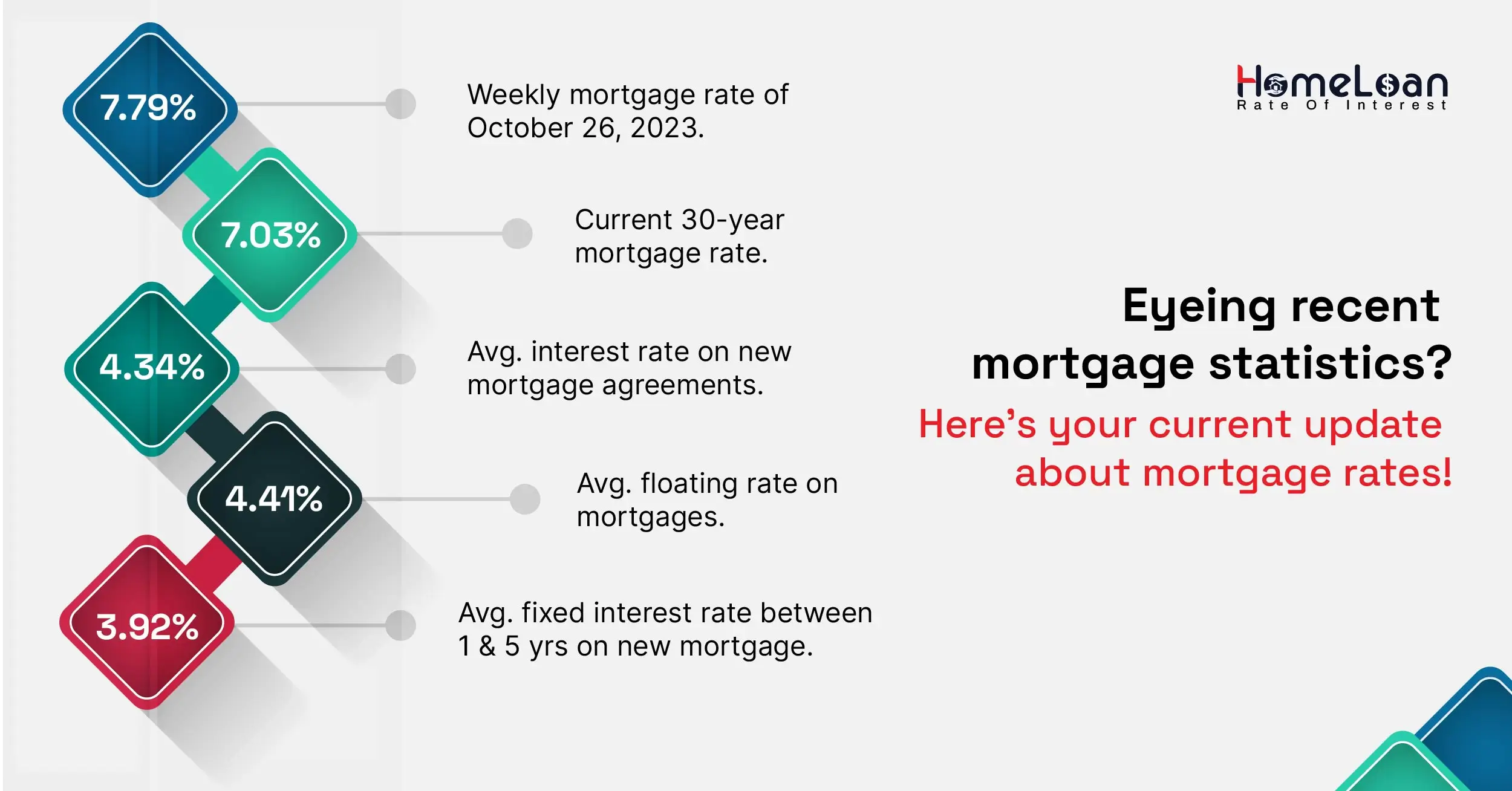

We know you’re eagerly waiting to check what’s in store for 2023. The good news is, as of December 12, 2023, the average nationwide rate was 7.32% for a 30-year fixed mortgage.

The 15-year fixed rate mortgage was on an average of 6.74%. But, this was not the case in early November. The above rates were 8.06% and 7.20% respectively.

Ultimately the Fed’s decision will be based on the current inflation trends. So, if the inflation is set to go down, mortgage rates inflation might also see a drop.

In 2023, the FED increased the mortgage rates due to higher inflation to reduce spending. This will lower inflation, as less money flows into the economy.

Get in touch with our mortgage representative at Home Loan Rate of Interest to find out if you can qualify for the 2024 mortgage interest rates.

Why should you watch out for the Fed’s decision?

You know that the mortgage rates inflation is not in your control. If you're wondering how the Fed's decision impacts your mortgage rates, keep reading to find out.

The Federal Reserve adjusts the federal funds rate, by buying or selling bonds and mortgage-backed securities. That's how you see an increase or a dip in your mortgage rates.

When the rates of federal funds are higher, financial institutions find it difficult to operate as it becomes expensive. To respond to this, institutions usually charge higher interest rates. This makes your mortgages more expensive than expected.

However, the Federal Reserve has made it clear that its focus is going to be on price stability and controlling inflation.

So, keeping this in mind, the Fed might continue to keep their rates, inflation and mortgage rates higher in 2024 as the inflation is still more than the target rate of 2%.

According to CBS News, there might be certain rate cuts in the federal funds during the second half of the year. If that happens, homebuyers can experience a drop in the mortgage rates.

Now that you know how your rates are fixed, it's time to prepare you to face inflation like a hero!

5 major effects of inflation on your finances

Before we get to the “how”, let’s understand the “what”. So, what exactly does inflation mean? In simple terms, inflation is the gradual increase in the price level of goods and services over time.

It's the silent force that has the potential to lower your purchasing power. From day-to-day products to services, the continuous rise of prices can strain your budget.

Probably wondering about how to protect your financial stability? Well, here are 5 really good tips to make saving super easy.

-

Make wise investment choices

Consider assigning a portion of your investments to assets that historically have shown resilience in spite of inflation.

Real assets like real estate and commodities often maintain or increase in value during inflationary periods, hence purchasing them can benefit you later.

-

It is good to expand your investment portfolio

Have a diversified investment portfolio by not just exploring a mix of stocks, and bonds, but also other assets such as precious metals (gold, silver, and platinum) as they have a higher degree of resiliency during a prolonged inflation time.

-

Review and adjust your budgets regularly

As you know, the cost of goods and services will fluctuate from time to time. So in order to cope with the frequent price changes, it is important that you adjust your budget at least once in 2 months.

-

Create an emergency fund

To deal with uncertain situations, it is important to build an emergency fund. They help you during the least expected times.

Without proper emergency funds, individuals might turn to credit cards or other forms of loans to cover unexpected expenses. This will ultimately lead to a debt trap.

-

Try to minimize your debt

Inflation will mainly hit your debt repayment capacity and become a burden on your monthly payments. This mostly happens when the interest rate on your debt is fixed.

So, it is advised to not take more debt than you can afford. By making monthly mortgage payments on time, you can reduce your exposure to higher inflation risk.

In a nutshell, inflation is not a buzzword. It happens in our day-to-day lives and it is important to plan ahead so that you are not drastically affected by inflation.

With the right strategy, we know that you can tackle inflation and mortgage rates in a snap! But hey, hang in there tight, as we highlight the tips for future homebuyers and current homeowners.

Why do people consider refinancing a good idea?

In recent times, more and more homeowners are choosing to refinance their mortgage because the demand jumps 14% and the rates fall to their lowest point.

According to the Mortgage Bankers Association, here are some of the refinancing trends that can help you decide -

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($726,200 or less) decreased to 7.17% from 7.37% including the origination fee for loans with a 20% down payment.

And that’s why, applications to refinance a home loan increased 14% from the previous week and were 10% higher than the same week one year ago.

Mortgage rates continued to move lower this week. The government’s all-important monthly employment report, expected to be released Friday, could either continue that trend or reverse it, depending on what it says about the state of the economy.

Matthew Graham, chief operating officer at Mortgage News Daily said - “November was a stellar month for mortgage rates, and December is picking up right where it left off.”

Homeowners, if you’re trying to refinance your mortgage, now looks like the right time to go for it!

4 upsides to refinancing your mortgage

We all know that a dip in the interest rates is an ideal time to consider refinancing. It helps you to take a breather and focus on managing your monthly payments. Based on what kind of loan you’re eligible for, refinancing has the potential to offer more than just one benefit.

With the interest rates at historic lows, homeowners can secure lower interest rates and they stand a chance to save thousands of dollars over the life of their mortgage.

A lower interest rate translates to more manageable monthly mortgage payments, which ultimately helps ease the strain on household budgets and provides financial flexibility.

When you refinance your mortgage, there are higher chances for you to consolidate the debts faster.

It also offers flexibility by allowing you to adapt to mortgage terms that align with your current financial objectives & circumstances.

2024 mortgage interest rates prediction

We know what you’re asking - will mortgage rates go down in 2024? Or will it continue to rise? Although we don’t have the exact mortgage rate predictions for 2024, we can share the influences behind fixing these rates.

Finding the best mortgage rates 2024 depends on the below factors and companies fix interest rates based on a pattern. Usually, they are offered to borrowers who have a great credit score, and have the ability to make a down payment of 20% or more.

Here you go, the 6 main factors that influence your interest rates include:

Your credit score and credit history.

Your financial situation.

Your down payment if you’re going to buy a home.

Your home equity if you’re planning to refinance.

Your loan-to-value ratio (LTV).

Your debt-to-income ratio (DTI).

And hey, remember this - don’t go in with the first quote you receive! Find out at least 3 to 5 quotes and compare them with what you can afford.

This will sound like a lot of work but trust us, if you set your mind to it, you can grab affordable interest rates and monthly mortgage payments.

Should you go for a mortgage in January 2024?

We agree that it’s too tough to bite the bullet especially when the mortgage rates inflation is higher. So, let the rates cool down a bit more so that you can get the best house at affordable mortgage rates.

Before moving forward, ask yourself these questions - Have you optimized your credit score? Do you have the right funds to make the required down payment?

This will help you understand your level of preparedness while entering the mortgage market in 2024. Don’t rush and lock the mortgage rates in the first month of 2024. Wait for some time, get your financial profile reviewed by the mortgage experts, and then decide.