- 15 Dec, 2023

Planning Your Retirement with Reverse Mortgages in California

Secure your retirement with a reverse mortgage in California

Are you a homeowner in California who’s at least 55 years old and looking for a way to utilize the equity you’ve built up in your home?

Then reverse mortgages are the right way to go about it! As Californian homeowners are entering retirement, many are looking for financial stability.

In today’s blog, you will learn about the strategic ways to plan your retirement with reverse mortgages in California.

How do reverse mortgages work?

If you’re used to making monthly mortgage payments, now is the time to start receiving those monthly payments with the help of reverse mortgages. We know you’re thinking - “how does a reverse mortgage work in California?”

The repayment for the entire loan balance becomes due if the borrower passes away, moves out permanently, or sells the home.

However, the loan is structured such that the amount doesn’t exceed the home’s value. To qualify for a CA reverse mortgage you need to meet the minimum age limit of 55 and the maximum age limit of 62 years.

💡Here’s a brownie point - The older you are, the higher the potential loan amount.

Types of reverse mortgages you can get in California

In case you’re wondering, there are 4 different types of CA reverse mortgages in California. You must understand the fundamentals of each type so that you can find the perfect fit based on your financial needs.

-

Home equity conversion mortgage (HECM)

This particular type of reverse mortgage in California is very common. These loans are federally insured and are offered to all borrowers who meet the age and home equity requirements.

The best part about this type of reverse mortgage is that there are no income requirements to successfully qualify.

Above all, there are absolutely zero restrictions on how you can use the borrowed money.

Consult with a counselor from the independent government-approved housing agency to explore the options. They will help you figure out the payment options involved, the fees, and other costs associated with the loan over time.

If you’re 62 or older, HECM is one of the good choices. If you have at least 50% of equity in your home, you can receive up to 40% to 60% of the value of your home’s equity.

-

HECM for purchase

This type of reverse mortgage purchase allows seniors aged 62 or older to purchase a new primary residence using the loan amount.

You’re lucky when it comes to repayment, as you get to choose to repay as much or as little as you prefer every month or make no monthly principal and interest payments.

This makes it easier for borrowers to focus on preserving more savings, and retirement assets while improving cash flow.

Using this, you get to buy a new home, pay a substantial down payment amount, and take out a CA reverse mortgage.

The total down payment that you are required to pay is determined based on the person’s age, home’s value, and the loan interest rate.

Here, you can purchase FHA-approved condominiums, single-family homes, townhouses, and manufacturing homes that meet HUD’s guidelines.

With this type of loan, borrowers can never owe more than the home’s value when the loan is repaid. This is called a non-recourse feature.

-

Proprietary reverse mortgage

They are private loans and they are not backed by the Federal government. They help homeowners who expect more money.

As they are not federally issued, they don’t require you to pay monthly mortgage insurance premiums.

If your mortgage balances are low, you qualify for more funds and as of the 2023 lending limit, your property must be more than $1,089,300 for federally backed HECMs.

It is good to research and compare the interest rates and fees from different proprietary reverse mortgage lenders.

This will help you gather quotes from different lenders and check which option will serve you best.

-

Single purpose reverse mortgage

Are you researching the least expensive CA reverse mortgages? The good news is that a single purpose reverse mortgage could be the right option.

The reason why they are not as expensive as other mortgage options is due to their usage. The amount borrowed can only be used for a single agreed-upon use.

They are offered by local or state government agencies or non profit organizations.

Individuals usually use a single purpose reverse mortgage to replace a roof, improve their water systems or pay taxes.

Homeowners who fall under the low to moderate-income category often find it difficult to qualify for other types of reverse mortgages. So, a single purpose reverse mortgage is specifically designed for these individuals.

Borrower rights of reverse mortgage California

The Department of Housing and Urban Development and the Federal Housing Administration offer enough protection to borrowers to reduce financial risks.

In addition to that, the State of California also offers unique opportunities and rights to homeowners safeguarding the interests of both the lenders and borrowers.

Now, let’s look at the rights Californians have:

-

Right to cancel

Once California homeowners complete all the counseling session requisites, they are granted 7 days before lenders file the application or charge any fees to homeowners.

-

Disclosures

Before the counseling session, lenders must provide the reverse mortgage worksheet guide and important notice to reverse mortgage loan applicants.

-

No annuities

Lenders cannot pitch annuities to homeowners and are prohibited from making a referral to annuity sellers.

-

Maintain the contract language

Lenders should provide all the contracts in the primary language of the borrower before the loan documents are sent for signature.

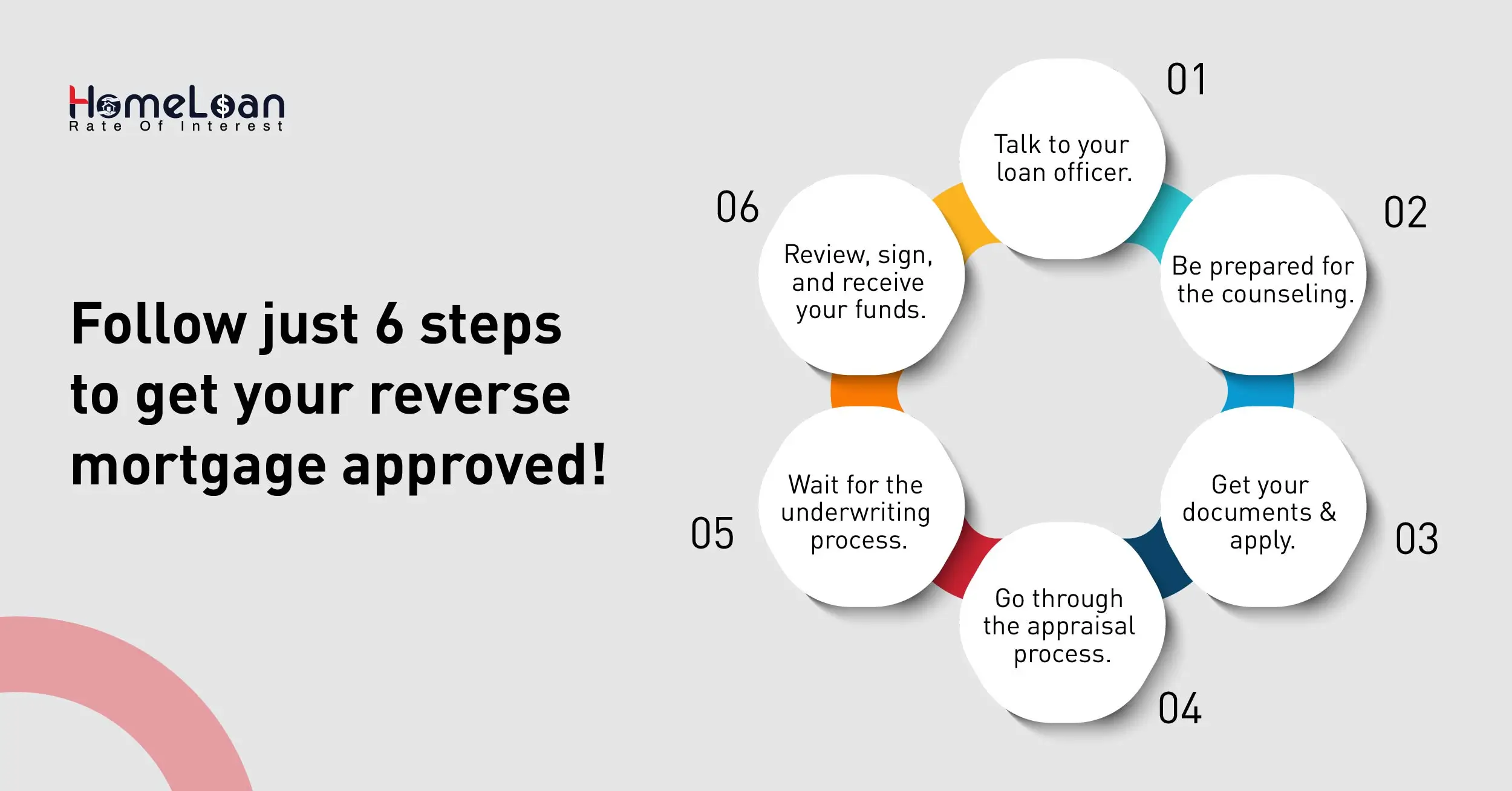

Step-by-step reverse mortgage purchase process

If you want to make the most out of the reverse mortgage loan, it is best to put on your waiting hats! The entire CA reverse mortgage purchase process can take about 30-45 days to get completed.

Here’s what your application process will look like👇

Step 1) You start talking to your loan officer

The primary step in your application process is to reach out to reverse mortgage loan advisors. They assess your complete financial situation and provide you with an estimate of reverse mortgage purchase benefits.

Step 2) You will undergo counseling

Once the financial review is completed by the loan officer, you will be attending a mandatory counseling session with a HUD-approved third-party counselor.

The session is aimed at educating you about the reverse mortgage features, level of suitability and other available options.

After the counseling session, you will receive a certificate that must be presented to the advisor before filing the reverse mortgage application.

Step 3) You need to file the application

Once your advisor reviews your counseling certificate, you will have to submit all the necessary documents with the help of your mortgage loan advisor.

These documents include all your government IDs, homeowner insurance policy and property tax bill.

Step 4) You will go through the appraisal process

Your lender will order a home appraisal to assess your home’s value while comparing the market value of your home.

This is done to determine the total loan amount that a borrower will receive once the loan is approved. Additionally, the credit score of the borrower also plays an important role during the appraisal process.

Step 5) Your loan will be processed and underwritten

The underwriting process begins once the application and required documents are received. Your underwriter will verify if you meet all the reverse mortgage requirements.

If they require additional information or home repairs before finalizing, they will raise a request. If everything is perfect your loan will be approved.

Step 6) Your application will be closed

Closing date will be scheduled by your lender and you will have to carefully review and sign the documents. Once done, your funds will be received after a mandatory waiting period of 3 business days.

We know it’s a long process but it is 100% worth waiting. If you want to further simplify your journey towards receiving the reverse mortgage funds, talk to us at Home Loan Rate of Interest and secure a peaceful retirement without any burden.

Meet these 7 reverse mortgage requirements

To qualify for the reverse mortgage California, make sure you tick off all these boxes before getting started.

You must be at least 55 years older. That’s a minimum requirement.

The home used against home equity must be the primary residence.

You must have equity in your home.

Your home must be maintained well in good condition.

You must continue to pay property taxes and homeowner’s insurance.

Your property must be eligible under the CA reverse mortgage standards.

You must complete a mandatory counseling session.

Expert advice and tips from HLRI

Pro Tip #1 - Engage with financial advisors who specialize in retirement planning and reverse mortgages in California. They can provide personalized advice based on individual circumstances.

Pro Tip #2 - Take advantage of online resources, including calculators, articles, and reputable websites, to enhance your understanding of Reverse Mortgages and retirement planning.

Ready for a great retirement?

A secure retirement is within reach when you approach it with a comprehensive plan that includes diverse income sources, thoughtful budgeting, and strategic use of Reverse Mortgages.

For Californians who are approaching retirement, the benefits of reverse mortgages are diverse. By taking the time to understand and seek expert advice, they can gain more and enjoy a more affordable retirement.