- 03 Jan, 2024

USDA Vs. FHA Loans - Which is right for you?

USDA loans Florida: eligibility, income limits, and everything you need to know

Are you looking to qualify for a USDA or an FHA loan and fulfill your dream of becoming a homeowner in 2024?

You have landed on the right blog! As a Floridian, you might have a lot of choices when it comes to the availability of financing options. But, there is always a question of which loan works best for you!

We have got your back. In today’s blog, we will provide you with enough information related to USDA loans vs FHA loans so that you can decide which one is right for you.

Recap of USDA & FHA loan basics

Foundation matters! Before understanding which loan type is the right one, it is important to know the key features of USDA loans Florida, and FHA loans.

First, we’ll dive right into the essential elements of Florida USDA loan 👇

-

USDA loans

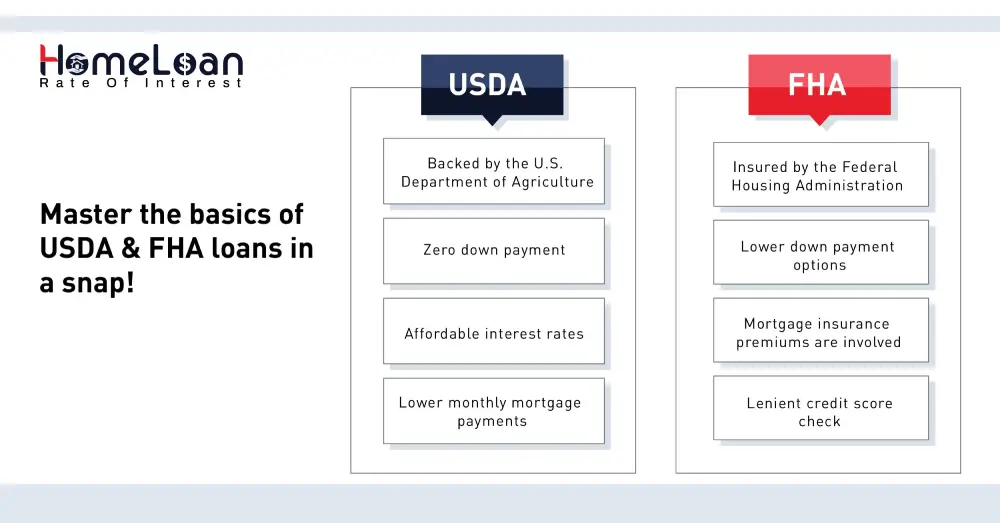

They are backed by the United States Department of Agriculture. This mortgage program is designed to facilitate homeownership for low-income residents of rural and suburban areas.

If you’re not able to qualify for a conventional loan, USDA loans in Florida can help you get a mortgage and buy that charming suburban home you’ve been eyeing.

The process to qualify for a USDA loan is not as complicated as it is for other mortgages. They are primarily focused on helping people who live in unhealthy or unsafe rural settings.

Contrary to common belief, these loans are not solely for farmers; they cater to a broader spectrum of homebuyers.

Additionally, USDA loans Florida also have a zero down payment advantage. Yes, you read that right!

Floridians can get a USDA loan and purchase a home with no down payment. This is a significant advantage, especially for first-time homebuyers or those with limited funds for a down payment.

Not only that, USDA loans in Florida also come with affordable interest rates, making them an appealing option for those who qualify. This means lower monthly mortgage payments throughout the life of the loan.

Alright, it’s time to have a quick run through the FHA loans.

-

FHA Loans

An FHA loan, insured by the Federal Housing Administration (FHA), is another government-backed mortgage program. They are insured by the government and issued by a bank that is FHA-approved

It aims to make homeownership more accessible by offering more flexible eligibility requirements and lower down payment options for borrowers with lower credit scores.

But, if you’re planning to go for an FHA loan, there are two types of mortgage insurance premiums that you need to pay. One is an upfront payment and the other is an annual payment.

Mortgage premiums are usually paid to offset the risk of loan defaulting as the borrowers come in with lower credit scores and down payments. That’s the reason lenders use MIPs to protect themselves from high-risk borrowers.

With all the essential information with us, let us explore the eligibility requirements, income limits, and the difference between USDA and FHA loans in Florida.

Eligibility requirements: FHA vs USDA loans in Florida

Whether you're drawn to the zero-down payment of USDA loans or the lower down payment of FHA loans, both options provide pathways to achieving the dream of owning a home.

But we need further information to refine our choices, right? Here are the eligibility requirements for you to make the best decision.

📸 P.S. Don’t forget to screenshot the table for future reference!

| Requirement type | USDA Loans | FHA Loans |

|---|---|---|

| Minimum down payment | 0% | 3.5% for credit score 580>= 10% for credit scores 500 to 579 |

| Minimum credit score | 640 | 500 |

| Income limits | Must have up to 115% of the median household income | No limits |

| Location requirements | Only available for USDA-eligible rural areas | None |

| Debt to income ratio | 41% of monthly debt payments | 43% of monthly debt payments |

| Upfront & annual fee | 1% guarantee 0.35% annual fee | 1.75% MIP 0.85% annual MIP |

| Property types | Single-family primary residence | 1 to 4 units of primary residence |

From this distinction, you can understand that USDA loans Florida have more stringent requirements compared to FHA loans.

But, the only difference is that FHA loans require you to pay an upfront down payment, unlike USDA loans. With that in mind, the next section is going to be about differentiating the key elements of USDA loan vs FHA loan.

Key differences between USDA loan vs FHA loan

Let’s take a look at the differences based on the application process, underwriting, appraisal process, interest rates, and mortgage insurance. This will help you determine the ideal loan option that can match your homeownership goals.

| Application process & underwriting | |

|---|---|

| USDA loan | FHA loan |

| The application process takes longer than an FHA loan as the underwriting is done by the lender first and then by USDA. | FHA loans usually take about 30 to 45 days to close based on the duration of underwriting. |

| Loan limits | |

| They don’t have a set limit but the maximum amount you receive depends upon your eligibility for a USDA loan. | These loan amount limits are set by the Department of Housing and Urban Development (HUD). It differs based on the low-cost areas and high-cost areas. |

| Appraisal | |

| They don’t have a set limit but the maximum amount you receive depends upon your eligibility for a USDA loan. | These loan amount limits are set by the Department of Housing and Urban Development (HUD). It differs based on the low-cost areas and high-cost areas. |

| Down payment | |

| You need not worry about a down payment with USDA loans Florida. | FHA loans do require a minimum 3.5% down payment if you maintain a credit score of 580. |

| Interest rates and mortgage insurance premiums | |

| You can expect lower interest rates as the USDA loans are backed by the government. Yet, they have an annual guarantee fee instead of a MIP. | FHA loans require borrowers to pay mortgage insurance premiums but the interest rates are still lower as they are also insured by the government. |

There you have it! Understand your requirements and weigh the differences accordingly! Next up in our blog is the application process for FHA & USDA loans Florida.

Step-by-step application process for USDA loans

Is the USDA loan the right one for you? Here’s a quick summary of the application process you must go through!

-

Prequalify with a USDA Lender

Start by identifying and reaching out to a USDA-approved lender.

Provide basic information and submit essential documents such as income statements, tax records, and employment history to determine your preliminary eligibility for a USDA loan.

The lender conducts a thorough analysis, including a credit check, to determine your eligibility and the potential loan amount.

Visit Home Loan Rate of Interest, apply, and get prequalified

-

Go house hunting for a USDA-eligible home

You can utilize USDA's eligibility map or consult with your lender to identify properties that qualify for USDA loans.

Ensure the chosen property is in a designated rural or suburban area, meeting USDA criteria.

-

Sign a purchase agreement

Once you've found a desirable home for yourself and your family, work with the seller to draft and sign a purchase agreement.

This agreement outlines all the terms and conditions of the home purchase.

-

Get underwriting done

Submit the signed purchase agreement and any additional required documentation to the lender.

The lender will then initiate your underwriting process by assessing your financial information and the property details.

Underwriting ensures that both you as the borrower and the property meet USDA loan requirements.

-

Wait for approval from USDA

Upon successful underwriting, your loan moves to the final approval stage, often referred to as "clear-to-close."

At this point, all conditions and requirements for the loan have been met, and the lender gives the green light for the closing process.

-

Sign and close

This is the final step and it involves signing the necessary paperwork to complete your home purchase.

You must review all the documents related to the loan, property ownership, and other legalities.

Voila! Once all documents are signed and funds are disbursed, you officially become a homeowner.

You need to be patient as the USDA loan application process requires collaboration with your lender and attention to detail at each stage.

Prequalification, pre approval, property eligibility checks, and the final approval stages are very important for a successful homeownership journey with a USDA loan.

Let’s now see what the application process is like for FHA loans!

Simplified process to apply for FHA loans

Securing an FHA loan involves a systematic process. Here's an overview of how your application journey will look like.

-

Check your eligibility

Use the above eligibility table to confirm that you meet the basic eligibility criteria for an FHA loan.

To give you a heads up, your eligibility includes factors such as a steady employment history, sufficient income, and a credit score that meets FHA requirements.

-

Find your ideal lender

Shop around for lenders who can offer competitive interest rates and lenient credit checks. Remember they should be FHA-approved!

Ensure that they offer 24/7 support and answer any questions you may have without hesitation. Also don’t forget to look for reviews and testimonials from other homebuyers.

-

Prepare the documents needed

Gather the necessary documents to support your loan application. Some of the common documents include proof of income, tax returns, employment history, and information about your debts and assets.

-

Complete your application

Submit the loan application with your chosen FHA-approved lender.

You need to provide accurate and detailed information to ensure a smooth processing of your application.

-

Get your appraisal done

Your lender will arrange for an FHA-approved appraiser to assess the value of the property you intend to purchase. This is done to ensure that your property meets all the FHA standards.

-

Close your loan

Once your application is approved, you move to the closing phase. Closely review all the documents and sign the necessary documents to finalize the loan agreement.

After closing is completed your lender will initiate the transfer of funds, and you officially become the owner of the property.

If you have made up your mind to apply for an FHA loan, there you go – This is what an ideal application process will look like.

Which is right for you - USDA or FHA?

If you’re an urban lover and a fan of city lights, FHA loans should be your choice. But, if you want to reside in Florida’s serene rural locality, USDA loans can offer you some amazing benefits.

So, you get to decide your desired place of living. Based on that, weigh your location preferences, and long-term goals.

As a final piece of advice, we urge you to reflect on your individual situations so that your decisions align with homeownership goals without any regrets in the future.